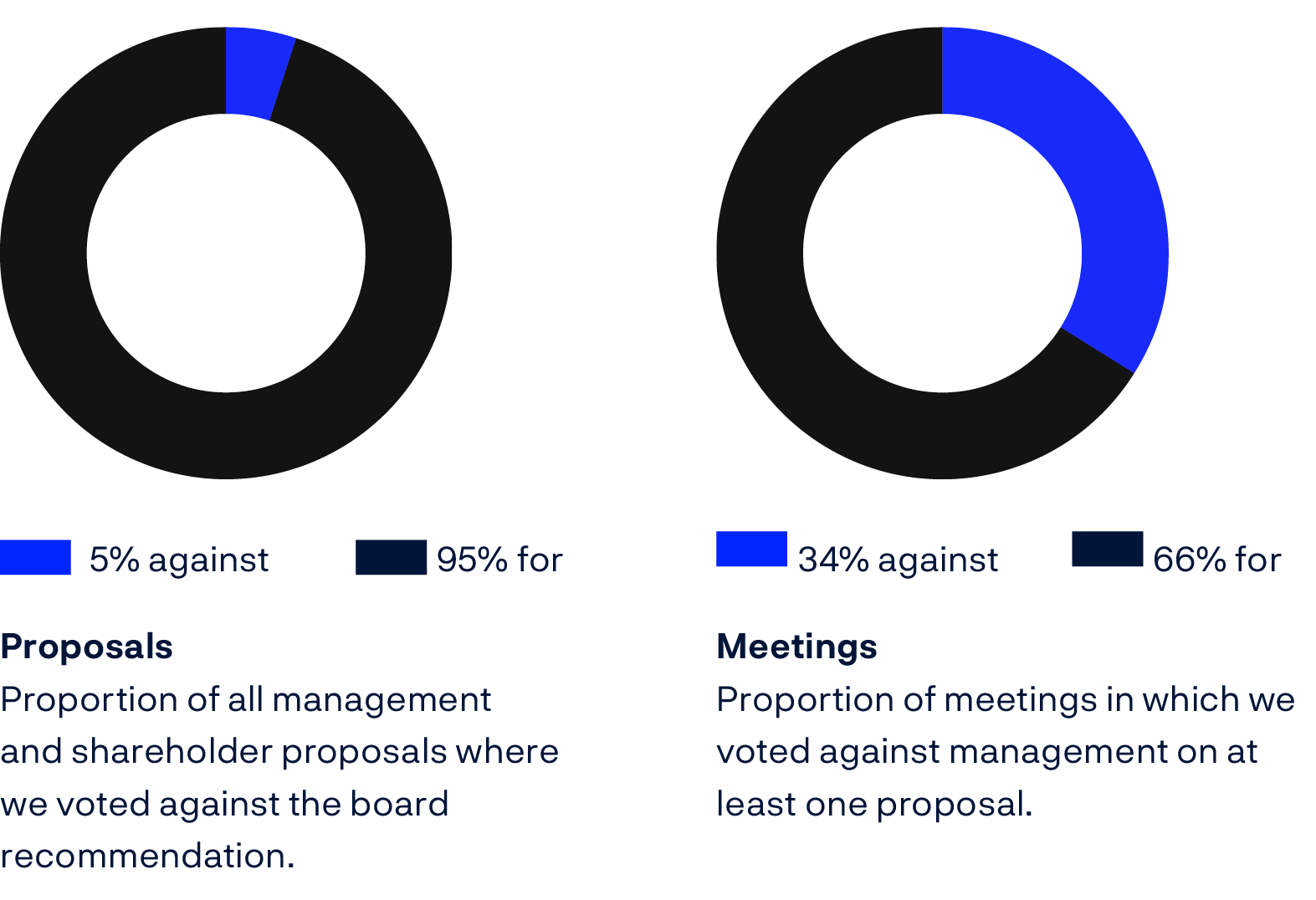

We voted at 8,522 shareholder meetings in the first half of 20231 and on a total of 94,731 proposals. Our voting is continuously updated on our website. In this review, we look at trends and outcomes, including on key topics like board composition and executive pay, and on shareholder proposals on a range of topics, including climate change and human rights.

Overall, we voted against the board recommendation on 5 percent of proposals and voted against at least one proposal at one third of company meetings. Concerns about board independence and the combination of chair and CEO roles continued to drive many of our votes against companies. Meanwhile, concerns about board gender diversity led us to oppose a small but growing number of companies. This trend looks set to continue as we expect to raise our expectations of the companies most misaligned with our position. We voted against around 1 in 10 CEO pay packages, including a growing number in the US, where our new framework aims to identify the pay structures we view as most problematic and misaligned with long-term value. We held more boards to account for material failures in the oversight, management or disclosure of sustainability risks, including considering social risks in a systematic way for the first time. Finally, shareholder proposals on sustainability topics continued to grow in breadth and prevalence, with a 15 percent increase in the number that we voted on, relative to 2022.

1Unless otherwise stated, all references to voting patterns in other years also refer to the period January – June in that year, for comparative purposes.

Our approach to voting

Through responsible investment practices we seek to increase the return and reduce the risk of the fund’s investments. As an active owner, we engage in discussions with management and boards of our portfolio companies to better understand and potentially seek to improve aspects of governance, including of material environmental and social matters, and of overall strategy and performance.

Our ownership gives us the right to vote at shareholder meetings on matters such as the election of board members, how executives are paid and aspects of capital structure, as well as on other topics proposed by shareholders.

Our general approach is to support the proposals put forward by management and supported by the board, on the basis that we participate in electing the board and entrust it with running the company.

However, we may vote against certain proposals, including the election of directors, where we consider that the board is not able to operate effectively, that our rights as a shareholder are not adequately protected, or that the company’s practices are materially misaligned with the principles expressed in our global voting guidelines. We may also vote in favour of proposals put forward by shareholders, which are not supported by the board and management. We consider these individually, against our decision framework.

Our voting guidelines are based on internationally recognised standards, such as the G20/OECD Principles of Corporate Governance, UN Global Compact, UN Guiding Principles on Business and Human Rights, and the OECD Guidelines for Multinational Enterprises. They are informed, in part, by the principles that we have expressed through our position papers on various governance topics, our expectations of companies on material sustainability issues, and our 2025 Climate action plan.

Our positions and expectations reflect the good practices that we wish to see companies adopt over time to reduce risks and increase value. We advocate for these in our dialogues with companies. Through our voting, we aim to address those companies most misaligned with these positions and expectations and move them towards these standards over time. Accordingly, our voting guidelines may include lower thresholds than our global expectations in certain areas, with the aim of raising these in future.

We aim to be consistent and predictable in our vote decisions, such that they could be anticipated by investee companies and explained by our voting guidelines and other documentation. To support this, since 2021, we publish our voting intentions five days before each meeting, with a brief rationale referring to the relevant part of our voting guidelines, whenever we vote against the board’s recommendations.

Being consistent and predictable does not mean that we vote the same way every year, on every issue, or even at every company. When applying our voting guidelines, we consider local market context and, where possible, company-specific circumstances, including insights from our portfolio managers, where we have a significant active holding in a company. Our internal portfolio managers have deep, company-specific knowledge. This is a strength when we vote. In 2023, portfolio managers participated in vote decisions for 661 companies, representing 58 percent of the value of our equity portfolio.

How we voted in 2023

We continued to support management and vote in line with the boards’ recommendations in most cases, however, we voted against management on least one proposal at around one third of meetings.

We support management in the majority of cases.

Some of the reasons that we voted against management were:2

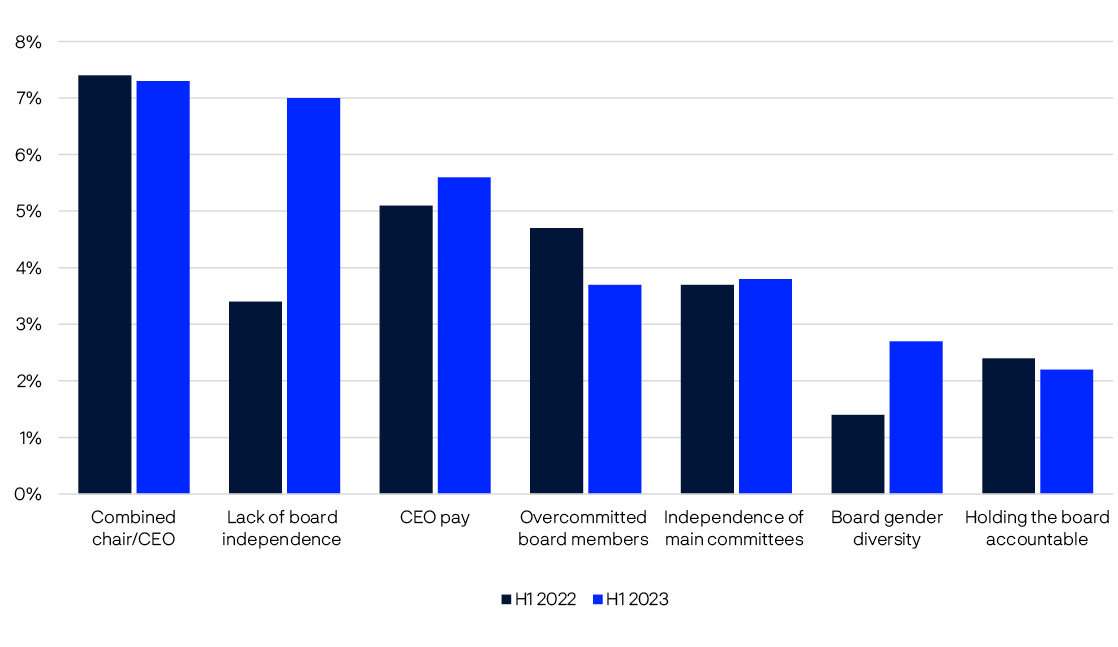

Board independence: one of the most common reasons we voted against companies was a lack of independence on the board, with our strengthened voting thresholds in Japan driving an overall increase, from 3 percent of companies in 2022 to 7 percent in 2023. See "Board composition and effectiveness" for more.

Combined Chair/ CEO roles: we continue to have concerns about the role of chair and CEO being held by the same person, with around 80 percent of all the companies we voted against for this reason being in the US and South Korea, where this structure remains relatively prevalent. See "Board composition and effectiveness" for more.

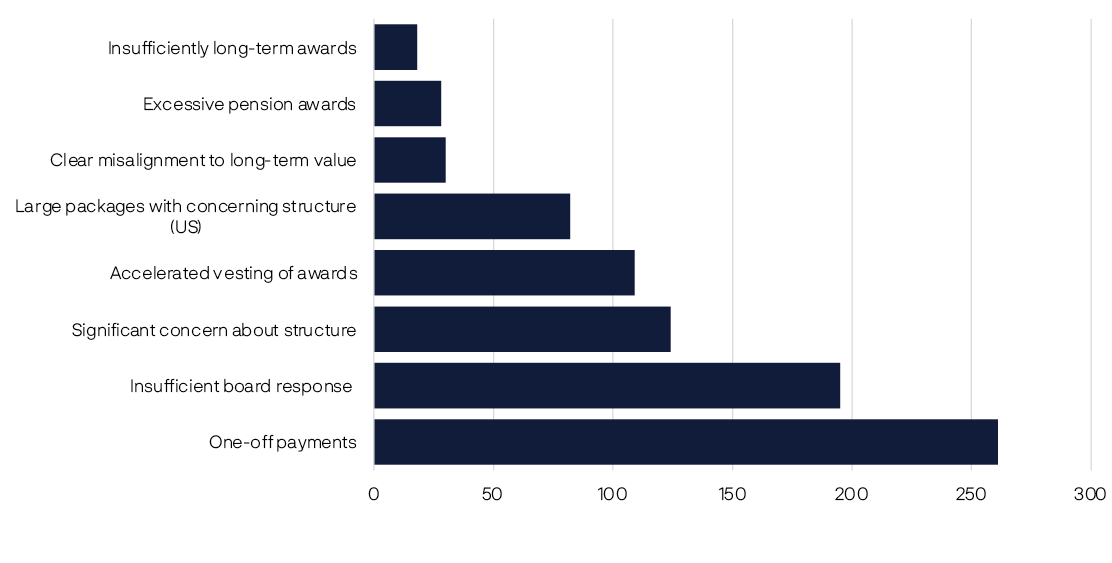

Concerns about CEO pay: we have long advocated for companies to adopt simple pay packages based on long-term share ownership for CEOs. Our vote policy aims to capture those companies most misaligned with our principles. This year, we voted against over 1 in 10 CEO pay packages. Overall, we voted against at least one proposal – including director elections – at nearly 6 percent of all companies based on concerns about CEO pay. The most common concerns were the use of one-off awards like ‘golden hellos’, awards that are paid out over too short a timeframe, and/or cases where we considered the board had not taken enough steps to respond to concerns from shareholders regarding pay in previous years. We developed a new framework for assessing US packages, leading us to vote against CEO pay at 82 companies where we assessed the package to be unduly costly and where we had significant concerns about structure out of a total of 142 US companies where we voted against CEO pay. See "CEO pay" for more.

Holding the board accountable: in a small but important number of cases, we vote against directors and/or boards where we believe they have failed to fulfil their duties. In the majority of cases (167 companies in 2023), this is related to governance concerns, such as where a company received low support for a pay proposal and we consider the board has failed to adequately address the issue; or where a company has experienced material failures of governance, risk oversight, disclosure, or a breach of fiduciary responsibilities. In recent years, we have expanded this to consider environmental and social factors, voting against directors where we consider there to be material failures in the oversight, management or disclosure of climate risks (19 companies in 2023), social risks (6 companies in 2023, when we introduced this consideration in a systematic way), or any other environmental risks (2 companies in 2023). The decision to vote against typically follows engagement with the company where we were not satisfied with the company’s response.

Board gender diversity: our global expectation is for each gender to represent at least 30 percent of the board, which we will implement through our voting guidelines over time (currently, we expect at least two representatives of each gender). This year, we voted against a relatively small but growing number of companies where the board failed to meet our voting guidelines, largely driven by our strengthened stance in Japan, where we began implementing this for the first time. See "Board composition and effectiveness" for more.

Shareholder proposals: Around 2 percent of the proposals we voted on were shareholder proposals, which we assess on a case-by-case basis. After careful consideration, we supported 48 percent of shareholder proposals in total; 52 percent of those relating to governance and 33 percent of those on sustainability topics. This included supporting the majority of those relating to lobbying and political contributions and a notable proportion of those relating to human capital management, human rights and climate. See "Shareholder proposals" for more.

Concern leading us to vote against companies in 2023.

Percentage of all companies we voted against driven by concerns on selected topics.

2See the appendix for a full breakdown of the reasons we voted against companies and how many companies we opposed.

Board composition and effectiveness

We generally own a relatively small percentage of the companies that we invest in, and we delegate most decisions to their boards and management teams. We expect board members to act independently and without conflicts of interest, to have the right balance of experience and skills to carry out their duties, and to be accountable for their decisions.3

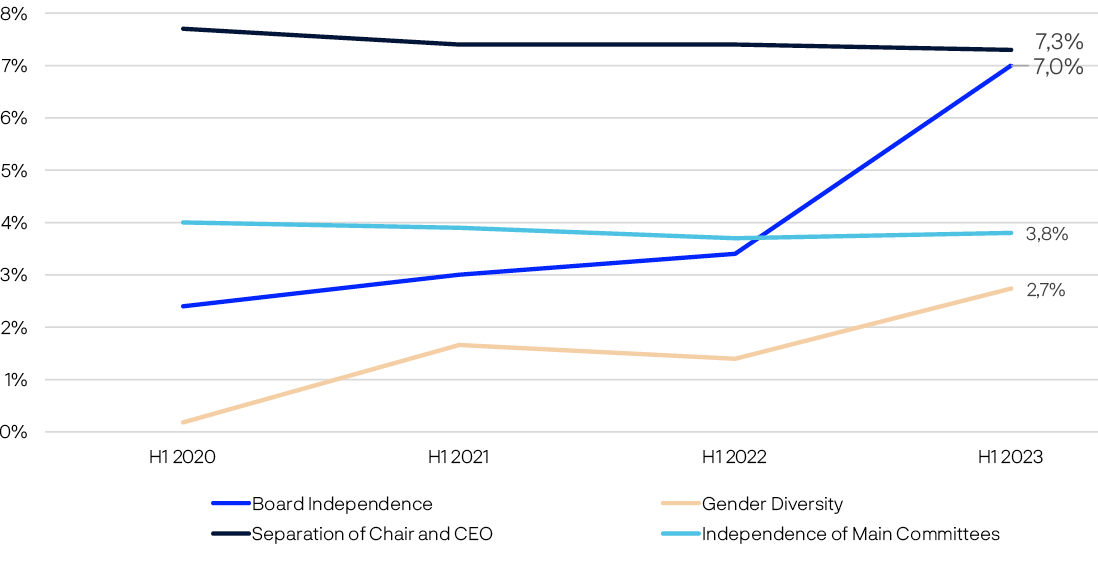

Concerns about board independence and gender diversity are driving a growing number of votes against companies.

The proportion of all companies we voted against due to concerns regarding a lack of board or committee independence, a lack of board gender diversity, and the roles of chair and CEO being held by the same person.

Board independence

We view board independence as a core component of good governance. In most markets, we expect at least half of board members to be independent, with some exceptions to this based on market context.

Overall, we are seeing some improvements to levels of board independence in developed markets, and we voted against

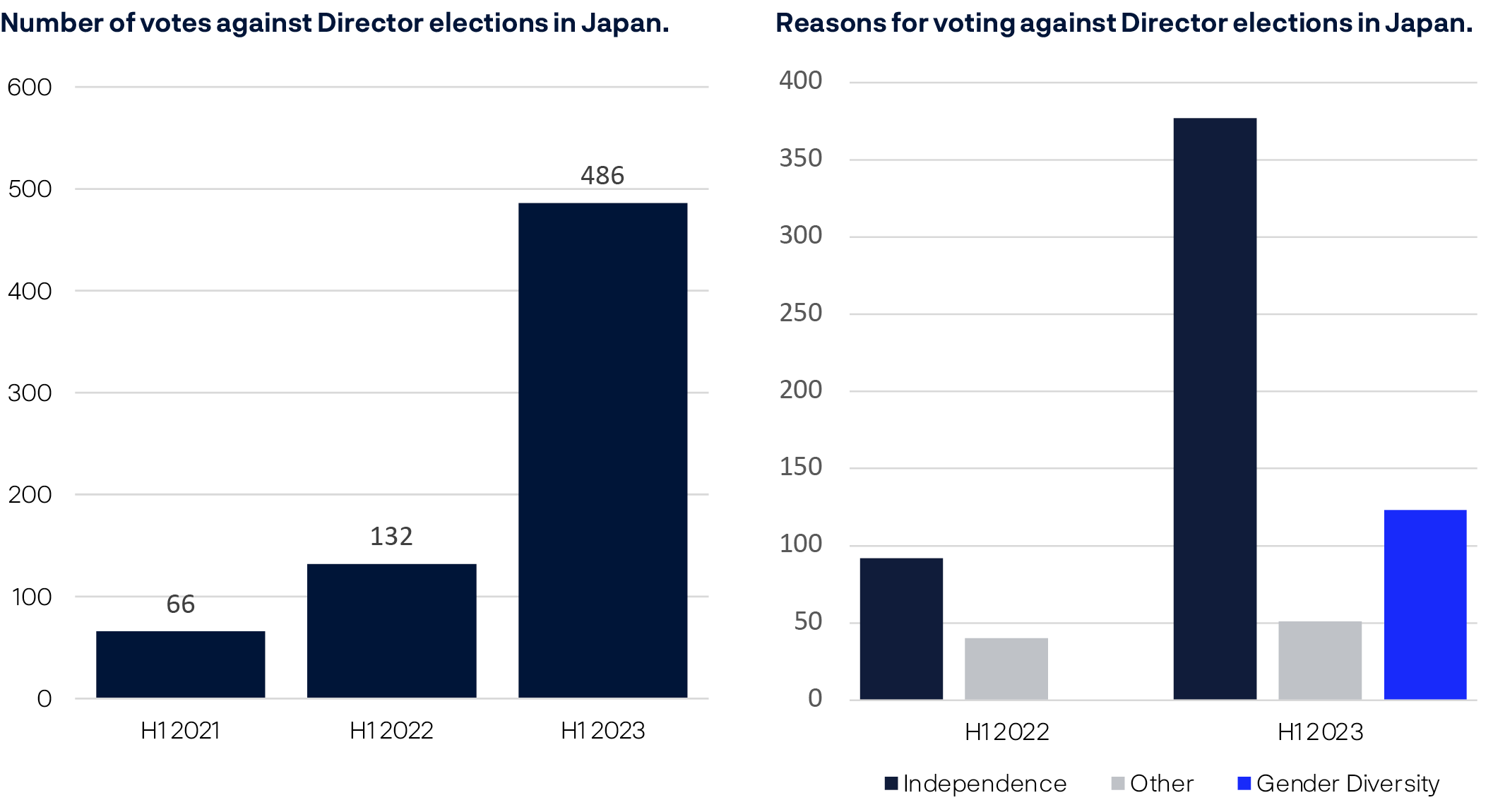

14 percent fewer directors or other relevant proposals than in 2022 due to insufficient independence. This does not include Japan, however, where a lack of board independence, as well as low levels of gender diversity, continue to be a concern. In 2023, we strengthened our voting guidelines for Japan to expect a minimum of one third independent directors on the board, up from a minimum of two directors. This led us to oppose 377 directors or related proposals due to board independence concerns, up from 92 in 2022. See "Independence and diversity in Japan" for more.

Separation of the roles of chair and CEO

One of the biggest drivers of our votes against companies was due to the roles of chair and CEO being held by the same person. We have long advocated for the separation of chair and CEO and believe that a non-executive chair is in a stronger position to guide strategy, oversee management and promote the interests of shareholders.

Markets where a combined role remains common include the US, where this concern contributed to us opposing the chair/CEO at 346 companies (around 20 percent of the US companies that we voted on), down slightly from 358 companies in 2022, reflecting relatively slow change on this issue.

We will continue to advocate for our portfolio companies to elect an independent chair and expect them to clearly demonstrate how any conflicts of interest are being mitigated in cases where separation is not considered to be feasible in the near-term.

Gender diversity

In the context of wanting to appoint effective boards with the diversity of skills, experience and perspectives necessary to fulfil their duties, we view having sufficient representation of each gender as an important indicator of board quality and decision-making.

Despite some progress,4 supported by regulatory and voluntary minimum standards for the inclusion of women in various markets around the world,5 women continue to be systemically under-represented on company boards.

Our expectation is that each gender represents at least 30 percent of the board. In our dialogues with boards that have not yet achieved this, we ask that they consider setting time-bound targets to do so. We have begun implementing this in our voting guidelines with a current guideline of at least two representatives of each gender in developed markets. We expect to increase this in the coming years.

Recognising that the dynamics that influence the representation of women on boards are heavily impacted by local market context, we make exceptions in certain markets. For example, in Japan, where levels of gender diversity have long lagged other developed markets, we introduced the expectation that boards include at least one woman from 2023 and will look to bring this in line with our global guidelines in due course.

Independence and diversity in Japan

Boards in Japan continue to lag those in other developed markets, in relation to levels of independence and gender diversity.

On Japanese boards, the term outsider is used to refer to board members who are non-executives. However, they may still be affiliated with the company and hence not independent. Various regulations and changes to market standards over the years have encouraged an increase in the proportion of independent directors. During the 2000s, a board composed entirely of insiders was the market standard, but by 2022, 82 percent of boards were at least one third independent and 63 percent had at least one female director.1 We welcome these developments and will continue to advocate, through our engagement with companies and our market-level work with standard-setters, for the transition to at least 50 percent independent boards and strengthened expectations on female representation, in-line with our global expectations.

We have progressively strengthened our voting guidelines for Japan to reflect these aims. In 2023, we moved from requiring at least two board members to be independent, to at least one third of the board, and will look to increase this in the coming years. Likewise, in 2023 we introduced a guideline for Japanese boards to have at least one female member and will look to bring this into line with our global guidelines in due course.

Our voting records from 2023 show that a notable proportion of our portfolio companies in Japan are not yet meeting our guidelines on board diversity (9 percent of Japanese companies in 2023) and/or independence (29 percent of Japanese companies in 2023), but we hope to see continued progress on these issues.

1 ISS 2022 Japan Proxy Season Review: https://insights.issgovernance.com/posts/2022-japan-proxy-season-review

3See our position papers on Board diversity, Board independence, Time commitment of board members, and Separation of chairperson and CEO

4The percent of female board members in MSCI ACWI Index companies increased from 17.9 percent to 24.5 percent between 2018 and 2022, Women on Boards Progress Report 2022 - MSCI

5For example, the 2022 European Directive requires EU-listed companies to have either 40 percent representation among non-executive board members or 33 percent representation of each gender amongst all board members by 2026.

CEO pay

How the management team of a company are incentivised and rewarded can have a significant influence over their decision-making and performance over time. It is particularly important in the case of the CEO. We advocate for simpler pay structures based on CEOs building up and holding shares for the long-term. We believe this most effectively aligns their interests with our own, as a long-term shareholder. It also reduces the risk of unintended consequences resulting from basing a significant portion of pay on achieving various performance metrics, given the difficulty in finding ones that sufficiently drive long-term outcomes.

Currently, relatively few companies around the world use a simple structure like the one that we advocate. Many use a combination of a cash salary with short and long-term incentive schemes, partly paid in cash and partly in shares, which are released to executives subject to a set of complex, multi-year criteria.

We do not think it would be constructive for us to oppose the majority of CEO pay packages, on the basis that they do not yet follow our preferred model. Therefore, in our voting guidelines, we set various limits that aim to identify the packages most materially misaligned with our preferred approach. For example, we will not support any pay packages that award CEOs shares over a time frame that we consider to be too short-term, or which include the use of substantial one-off awards (such as ‘golden hellos’ and severance payments). We will also vote against packages which appear unduly costly and where we have concerns about the overall design of pay schemes and/or the alignment with performance. Finally, we consider whether boards have appropriately responded to shareholder concerns about pay in previous years.

In 2023, we voted against CEO pay packages at over 1 in 10 companies, more than in recent years and in part driven by concerns about pay in the US and a tightening of our voting framework. See "CEO pay in the US" for more.

Reasons that we voted againt CEO pay in 2023. Number for companies opposed.

CEO pay in the US

CEO pay levels in the US are some of the highest in the world and have risen significantly since the 1980s. Average pay for employees has not kept pace with that of CEOs, with the average CEO to worker pay ratio rising from 20 to 1 in 1965, to 399 to 1 in 2021. Although the US is home to many of the world’s most valuable companies, evidence suggests that higher CEO pay levels are not necessarily correlated with higher performance.1,2

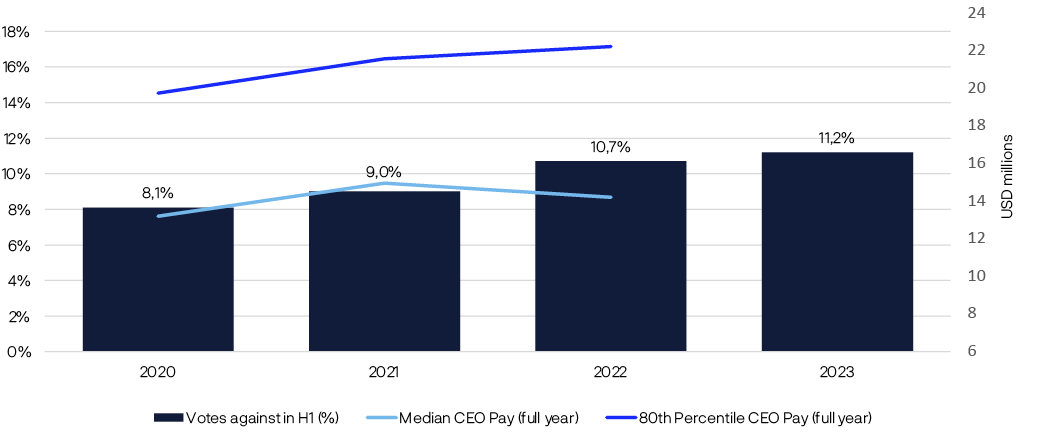

We are voting against more US pay packages as pay levels continue to rise.

Proportion of ‘say-on-pay’ proposals in the US that we voted against, relative to median and 80th percentile US CEO pay amongst Norges Bank Investment Management portfolio companies3. Note that ‘say-on-pay’ votes typically relate to pay awards over the previous year.

We are using a new framework for evaluating US packages, looking at absolute value, peer comparisons and dilution. We do not vote against pay packages based on size alone. Our aim is to identify the structures we view as most problematic and misaligned with long-term value. For 2023, we applied this stricter assessment to packages worth 20 million dollars or more, leading us to vote against more than half of packages above this level.

‘Say-on-climate’ proposals

Climate change is one of the defining challenges of the 21st century. As a diversified, global investor, the fund would benefit from an orderly transition in line with the goals of the Paris Agreement. We expect companies to manage climate risks and opportunities in a manner that is meaningful to their business model and situational and context. We expect companies to set net-zero and interim decarbonisation targets, define strategies to achieve these, and be transparent about their approach.

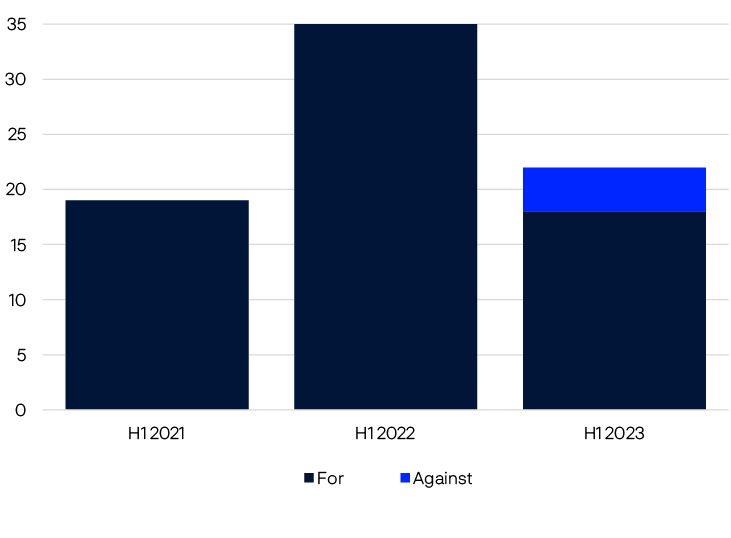

An increasing number of companies are asking their shareholders to approve their climate plans. In most cases, these ‘say-on-climate’ votes are non-binding and advisory. This is still a relatively new field, and good practice for what climate transition plans should contain is still under development.

When voting on climate plans, we consider elements such as the ambition level of targets set, the robustness of the plans, and the detail of related disclosures. Where we do not believe plans to be sufficiently developed or coherent, we will not support them, as was the case with 4 of the 22 proposals we voted on in 2023.

We do not believe that direct shareholder approval of a climate plan is always necessary or supersedes the board’s responsibility for ongoing oversight of climate change. Where shareholder approval is sought, it is likely that seeking shareholder approval periodically – for example, every three years – rather than every year is sufficient, given the strategic nature of such plans. Any material changes made outside of this cycle should nevertheless be brought to shareholders.

'Say-on-climate' proposals.

The numbers of ‘say-on-climate’ proposals put forward by management teams and the proportion of these that we voted for and against.

Shareholder proposals

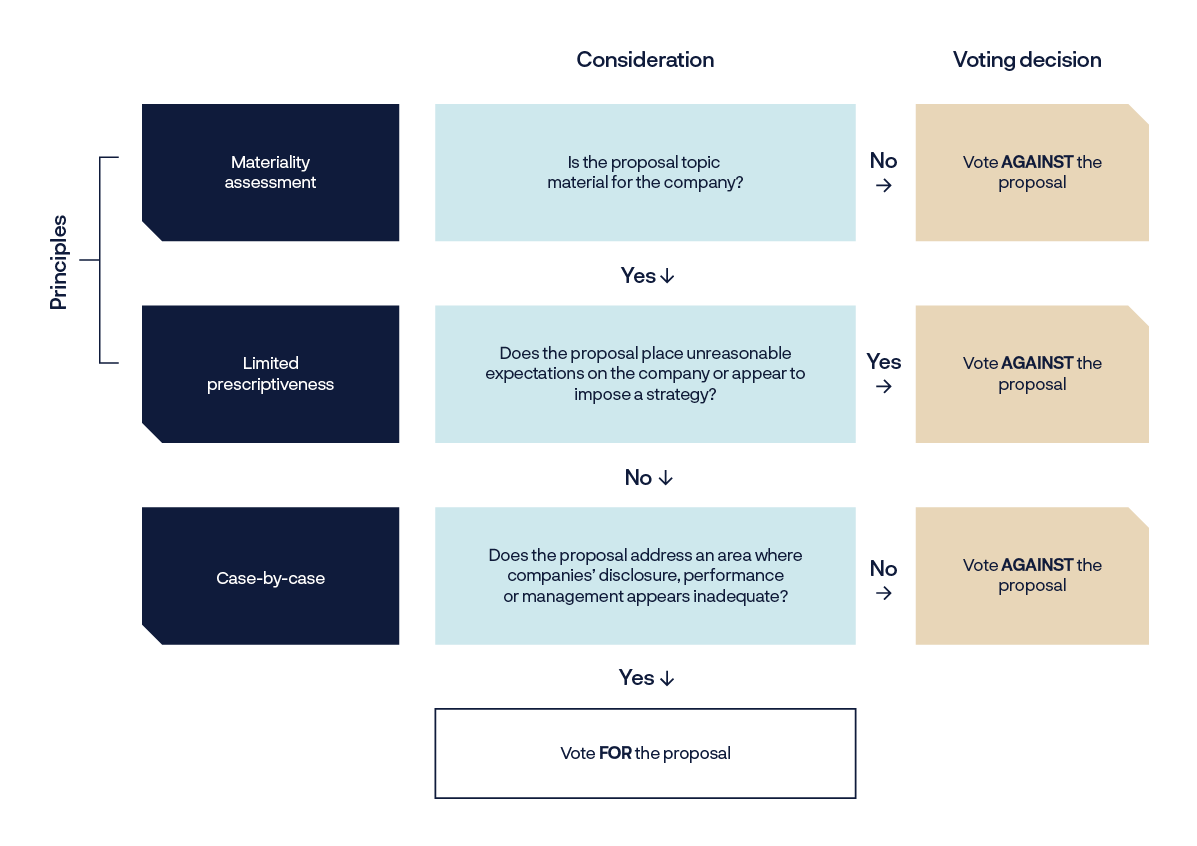

We believe shareholder proposals can be a useful tool for holding boards accountable in cases where a company lags market standards, where the majority of shareholders disagree with specific strategies of the company, or where a proposal aligns with our positions or expectations, and we do not believe a company is taking sufficient action to meet them.

We evaluate each shareholder proposal individually, drawing on our in-house expertise on governance, environmental and social topics, as well as current research and market trends, to reach an informed voting decision. We follow a three-stage framework in reaching our decision, considering first the materiality, then the scope, and finally the prescriptiveness of a proposal. This is discussed further in our Responsible investment report 2023 and in our paper on sustainability shareholder proposals.

We may also choose to file or co-file shareholder proposals in select cases where we believe this to be appropriate, for example, where we do not believe a company has responded sufficiently to our engagement dialogue on an issue material to long-term value. See: "Norges Bank Investment Management 2023 shareholder proposals" for more.

In 2023, the majority (79 percent) of shareholder proposals that we voted on related to governance. The remaining 21 percent of proposals related to environmental and social topics, with the numbers of proposals on these topics rising year-on-year (416 in 2023, vs. 361 in 2022).

In particular, the number of environmental and social-related shareholder proposals at US companies continued to grow,6 with topics as varied as labour rights, access to vaccines, animal welfare, stranded asset risks, and fossil fuel funding. The commentary around these proposals becomes increasingly politicized in some markets and the number of proposals filed by so-called ‘anti-ESG’ proponents7 nearly doubled year-on-year, rising to nearly 10 percent of all proposals.8 We will continue to assess these on their merits, looking carefully at the company’s context and using our assessment framework, including considering the extent to which the intended outcomes are aligned with our ownership principles, as well as our stated positions and expectations. In practice, we overwhelmingly voted against such proposals based on this approach.

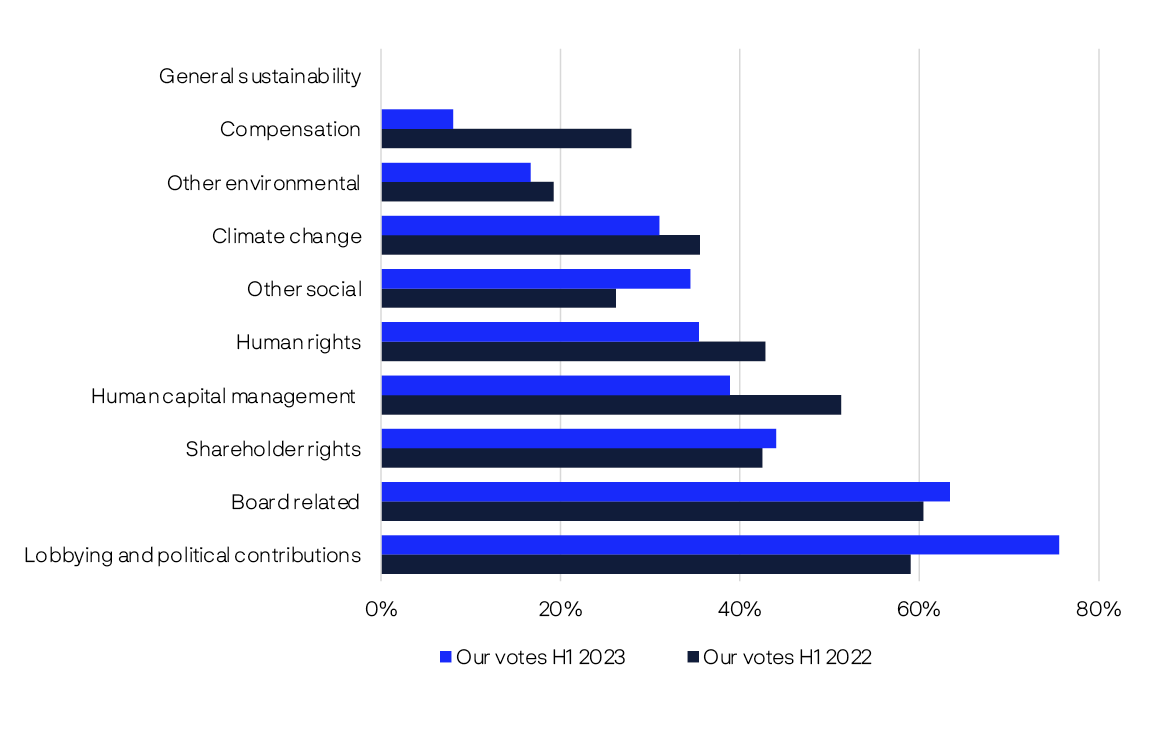

Our support for shareholder proposals has remained relatively flat this year compared to 2022, albeit with some differences at the topic level. For example, our support for shareholder proposals related to lobbying and political contributions, board-related proposals, and shareholder rights all increased during the first half of 2023. In particular, we supported a relatively high proportion of proposals relating to better disclosure of lobbying and political contributions, and this number has increased since 2022 as we have strengthened our expectations of corporate disclosures in this area.

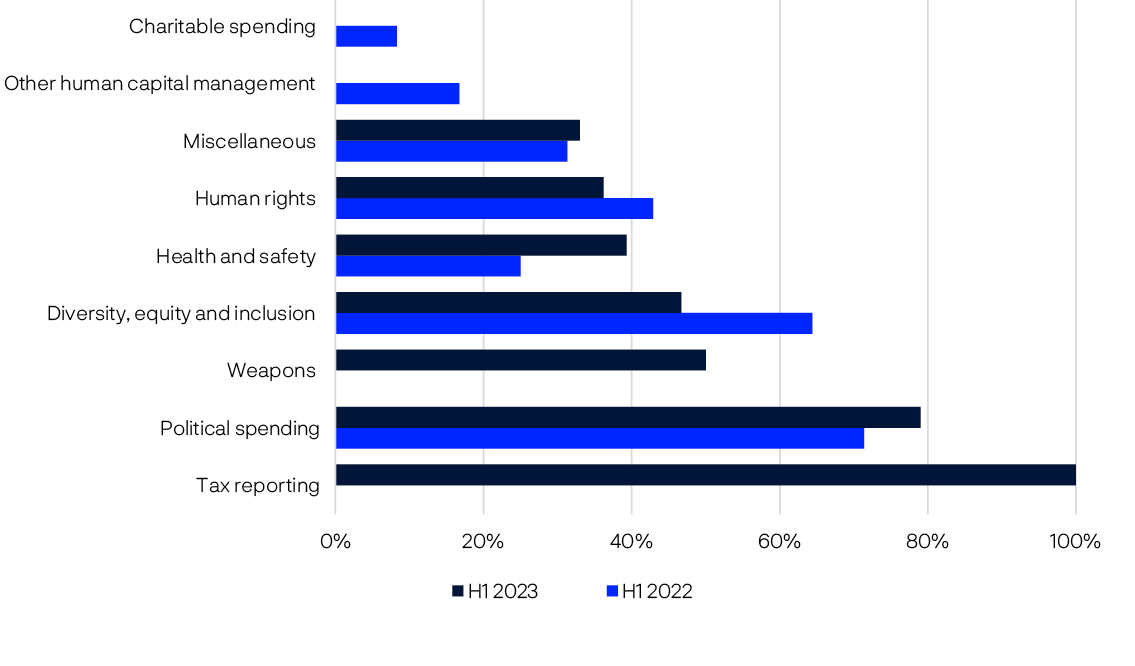

Support for shareholder proposals.

The proportion of shareholder proposals that Norges Bank Investment Management supported, by high-level topic.

When looking at our level of support for different categories of proposals, it is important to note that our vote decisions are driven by the specific demands and wording of resolutions (prescriptiveness) and the specific circumstances of the companies at which they are filed (scope). They do not solely reflect the importance we place on the topics the proposals refer to (materiality). For example, we supported fewer shareholder proposals relating to climate change this year, relative to 2022, but climate risk remains a priority for the fund.

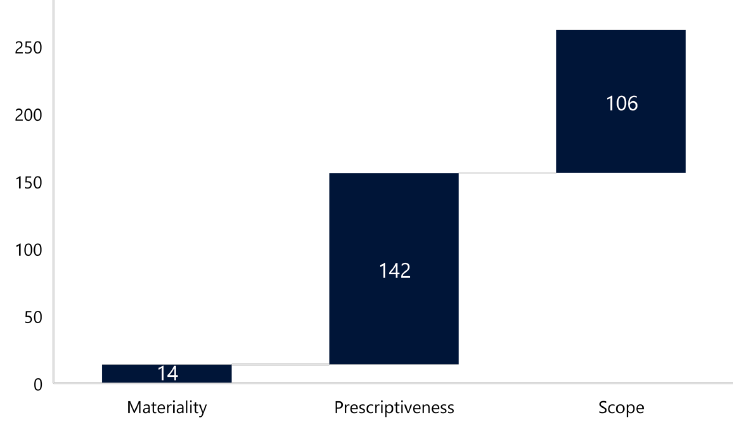

This year, in the majority of cases where we opposed a shareholder proposal on environmental or social topics, it was due to concerns about its prescriptiveness or scope.

Reasons we opposed environmental and social shareholder proposals in 2023. Number of proposals.

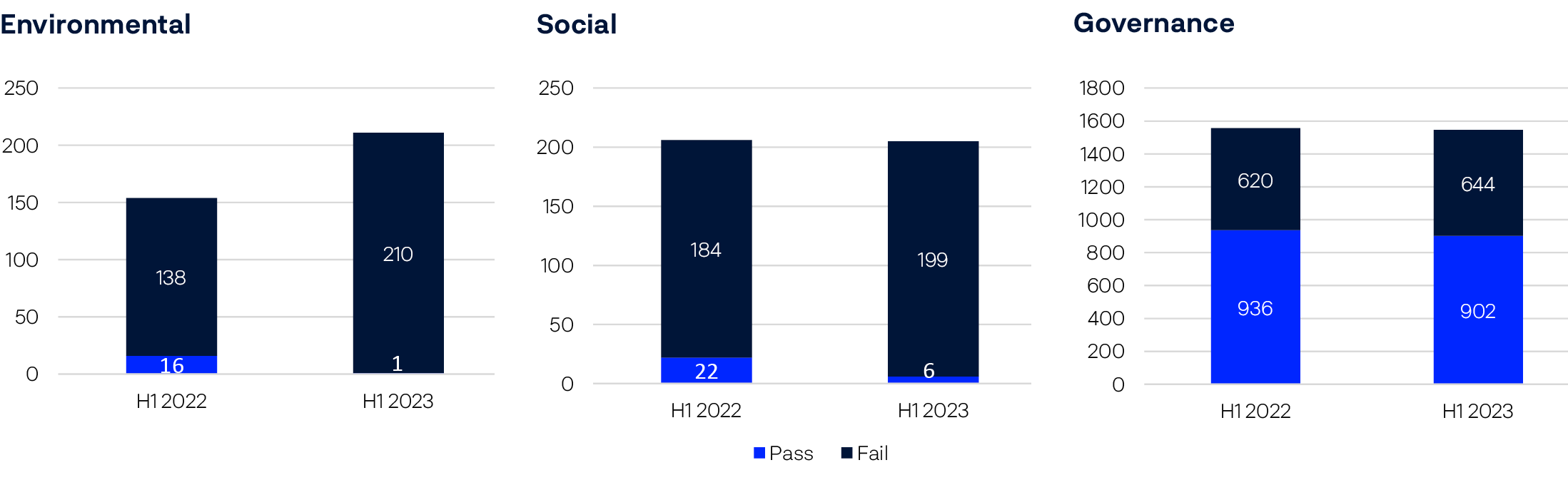

We saw a decline in support from other investors across all environmental, social and governance topics,9 with the overall number of proposals on environmental and social topics that were approved dropping from 38 in the first half of 2022 to 7 in the first half of 2023.10 This may reflect investors’ varying thresholds for materiality, scope and prescriptiveness, as well as an increasingly politicized ESG-environment for companies and investors alike in some markets.

The proportion of shareholder proposals that passed, by category.11

Environmental topics

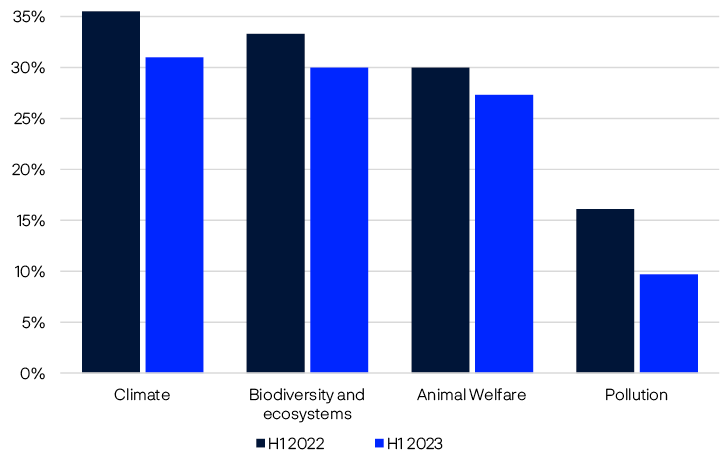

This year, we saw shareholder proposals on a range of environmental issues, with topics ranging from animal welfare to calls for an end to fossil fuel funding, reporting on a just transition and stranded asset risks. Although we supported fewer proposals than in 2022, we continued to support nearly one third of proposals relating to climate or biodiversity and ecosystems.

Our support for shareholder proposals on environmental topics, by sub-topic.

As stated in our 2025 Climate action plan, we believe that the fund benefits from an orderly transition towards global net zero emissions that fully addresses the risks associated with climate change. We expect company boards and management to implement net zero plans. The climate transition happens over decades, differs across markets and industries, and depends on the board and management making complex decisions based on future physical, regulatory and technology scenarios. Our active ownership goals therefore require engagement with companies over a longer period of time and may lead us not to support overly prescriptive shareholder proposals, such as those requiring a ban on financing all fossil fuels over a relatively short time frame, that may not be in the best interests of a company or the energy transition.

Nonetheless, we will take action where we believe companies are materially misaligned with the aims of our Climate action plan, and this year, we filed our own shareholder proposals relating to climate for the first time.

Norges Bank Investment Management 2023 shareholder proposals

In 2023 we filed shareholder proposals where we asked four high-emitting companies in the US to establish or strengthen their emission reduction targets. This was the first time we filed shareholder proposals on a sustainability issue.

We met with the companies to discuss our proposals, and we withdrew our proposals to Packaging Corp of America and Marathon Petroleum following constructive dialogue and commitments by the companies to strengthen their targets. According to the proxy advisor ISS, 42 percent of shareholder resolutions on sustainability in the US were withdrawn ahead of the AGMs in 2022.

Our proposals to NewMarket Corporation and Westlake Corporation were voted on by the companies’ shareholders and gained 28 percent support at NewMarket Corporation and 11.5 percent support at Westlake Corporation. The latter is a company where the majority of the shares are controlled by one family, which means that the support from the independent shareholders was significantly stronger.

We believe that the strong support by independent shareholders sends a clear signal to the companies about the materiality of climate change and the need to set emissions reduction targets.

Social topics

This year saw a notable increase in the number of proposals relating to human rights and human capital management, with 81 proposals in the first half of 2023 vs. 51 in 2022 and 9 in 2021. Topics included calling for additional reporting and human rights impact assessments, freedom of association and collective bargaining. We supported 37 percent of these proposals this year, after careful assessment.

Transparency on lobbying and political contributions and the extent to which these align with companies’ stated positions on various social topics, as well as on climate, has continued to be a significant topic this year. We supported the majority (76 percent) of proposals this year, up from 59 percent in 2022, as we strengthened our expectations of companies in this area.

Other key topics were gender and racial pay gap reporting, with nearly twice as many proposals this year, of which we supported all; and health and safety, with an increase from 24 to 29 proposals this year, including 11 on reviewing of drug pricing or distribution and 6 on reporting on health care reform.

Our support for shareholder proposals on social topics, by sub-topic.

6https://corpgov.law.harvard.edu/2023/06/01/2023-proxy-season-more-proposals-lower-support/#:~:text=Aspercent20wepercent20predictedpercent20inpercent20our,2022percent20percentE2percent80percent93percent20apercent2069percent20percentpercent20increase

7https://corpgov.law.harvard.edu/2023/06/01/anti-esg-shareholder-proposals-in-2023/#:~:text=Generally%20speaking%2C%20the%20anti%2DESG,their%20social%20and%20environmental%20impacts

8https://images.info.computershare.com/Web/CMPTSHR1/percent7Ba71e7ae0-76c4-4d02-92bd-b8836254bf4epercent7D_Georgeson-US-Early-Proxy-Season-Report-2023.pdf

9https://corpgov.law.harvard.edu/2023/06/01/2023-proxy-season-more-proposals-lower-support/#:~:text=Aspercent20wepercent20predictedpercent20inpercent20our,2022percent20percentE2percent80percent93percent20apercent2069percent20percentpercent20increase.

10ISS data

11ISS data

|

Concern leading us to vote against companies (all topics) |

Percentage of companies opposed |

|

|---|---|---|

|

H1 2023 |

H1 2022 |

|

|

Combined chair/CEO |

7.3 |

7.4 |

|

Lack of board independence |

7.0 |

3.4 |

|

CEO pay |

5.6 |

5.1 |

|

Financial statements |

4.5 |

4.6 |

|

Independence of main committees |

3.8 |

3.7 |

|

Overcommitted board members |

3.7 |

4.7 |

|

Board nomination and election |

2.9 |

3.2 |

|

Changes to bylaws or charter |

2.7 |

3.7 |

|

Board gender diversity |

2.7 |

1.4 |

|

Auditor |

2.5 |

2.0 |

|

Holding the board accountable |

2.0 |

1.9 |

|

Anti-takeover measures |

1.6 |

1.8 |

|

Sustainability reporting |

1.3 |

1.0 |

|

Share issuance |

1.3 |

1.5 |

|

Related party transactions |

1.1 |

1.1 |

|

Mergers, acquisitions and other corporate transactions |

0.3 |

0.4 |

|

Multiple share classes |

0.3 |

0.2 |

|

Meeting requirements |

0.1 |

0.1 |