1. Introduction

2024 highlights

We made progress in line with our 2025 Climate action plan. We made further renewable energy investments. We increased our transparency and received recognition for these efforts. CEO pay remained a priority for us and we advocated for simpler and longer-term incentives. To mitigate financial risk for the fund, we divested from companies with unsustainable business models.

Delivering on the 2025 Climate action plan

A core part of our 2025 Climate Action Plan is to engage with the highest emitters in our portfolio on how they can achieve net zero emissions by 2050. We want to support our portfolio companies in delivering long-term financial value and adapting their business models towards achieving this ambition. In 2024, we engaged with 141 companies as part of our net zero dialogues, accounting for 46 percent of the fund’s financed emissions. In total, climate change was raised in meetings and correspondence with 480 companies, accounting for 54 percent of financed emissions.

Our 2024 Climate and nature disclosures look at the financial climate and nature-related risks and opportunities facing the fund and provide detailed information about the progress on our climate action plan.

74 percent of financed emissions covered by net zero 2050 targets. Overall 32 percent of the companies in the portfolio

43 percent of real estate portfolio aligned with a 1.5C decarbonisation pathway

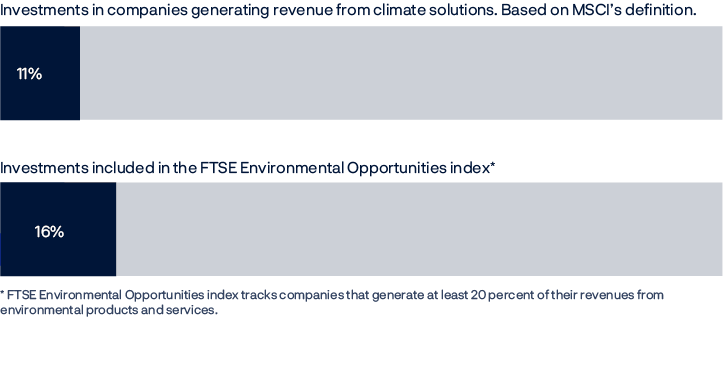

11 percent of equity portfolio invested in climate solutions (MSCI Low Carbon Transition Score)

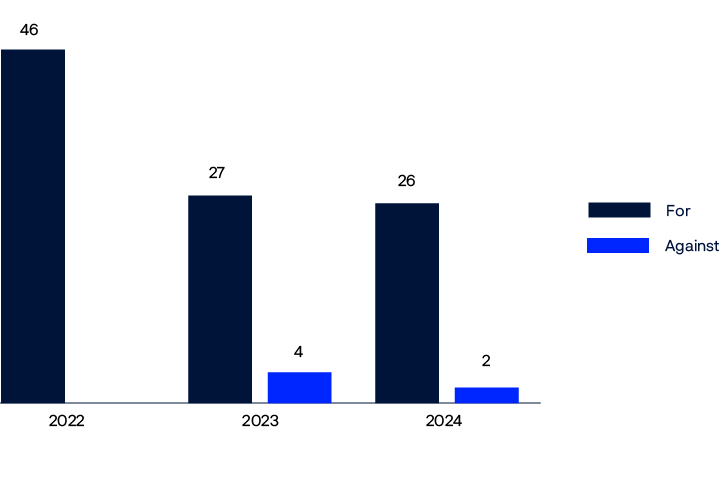

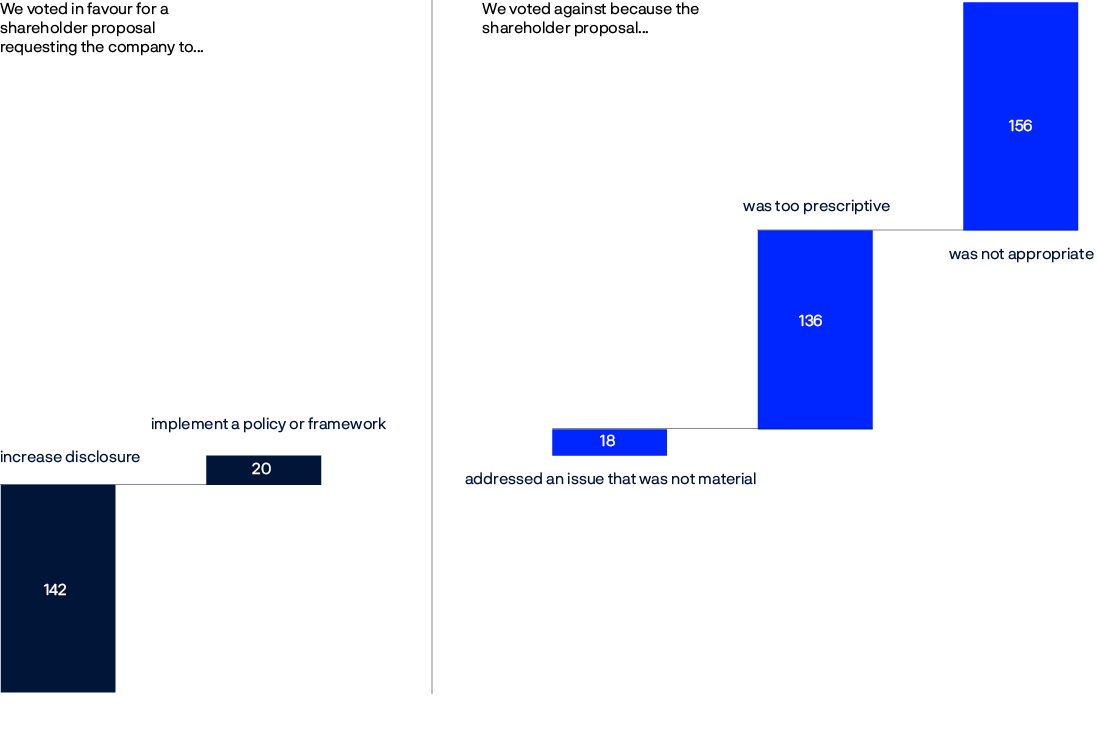

3 shareholder proposals filed

Increasing voting and ownership transparency

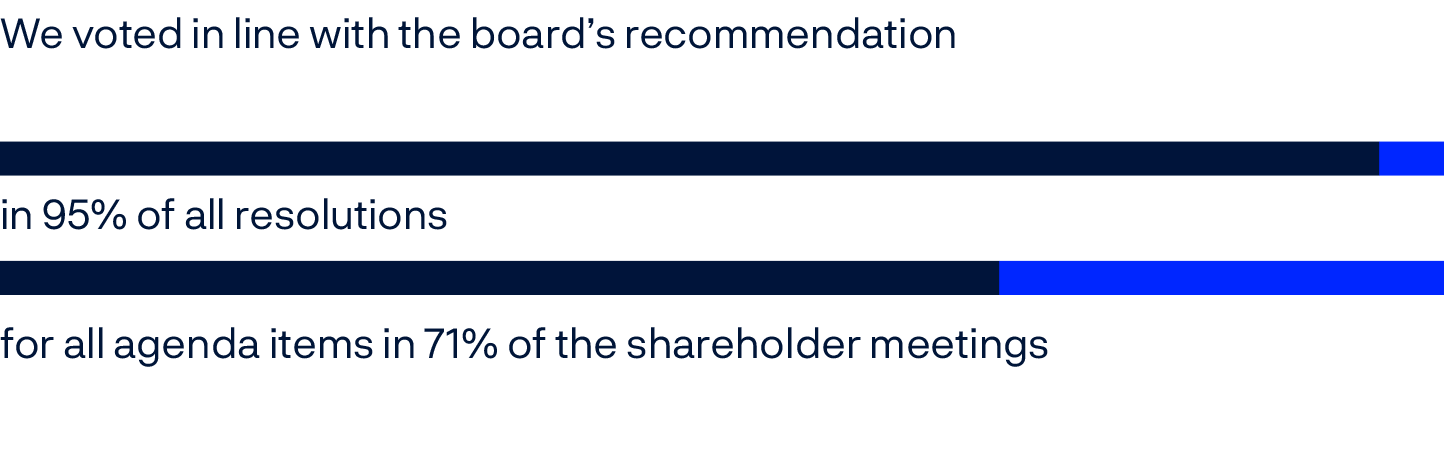

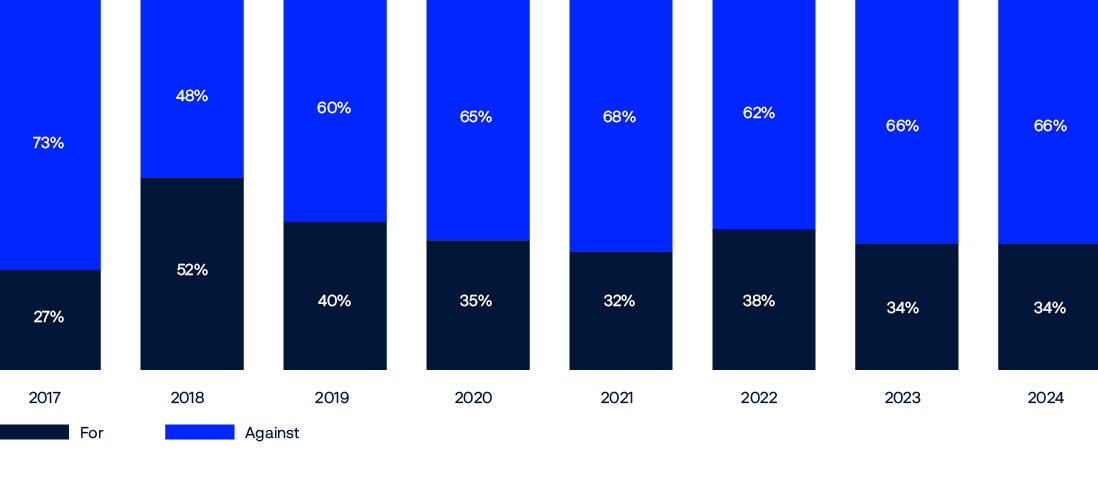

Transparency about the management builds trust and knowledge about the fund, both in Norway and internationally. In 2024, we started sharing our voting intentions through the Bloomberg voting platform and communicated more detailed rationales for selected votes for the first time. We published an annual voting review and continued disclosing our voting intentions five days before the shareholder meeting. We explained when we voted against proposals supported by the board or when we opposed shareholder proposals.

We were recognised as the world’s most transparent fund in the Responsible Investing category by the Global Pension Transparency Benchmark and received the International Corporate Governance Network Global Stewardship Disclosure Award for our commitment to transparency and reporting.

110,656 votes at 11,154 shareholder meetings

3,313 company meetings

30 consultation responses

Diversifying our investments in renewable infrastructure

Our mandate opens for investments in renewable energy infrastructure. These are financial investments, and our renewable infrastructure investment strategy focuses on acquiring high-quality assets that offer sustainable, long-term returns.

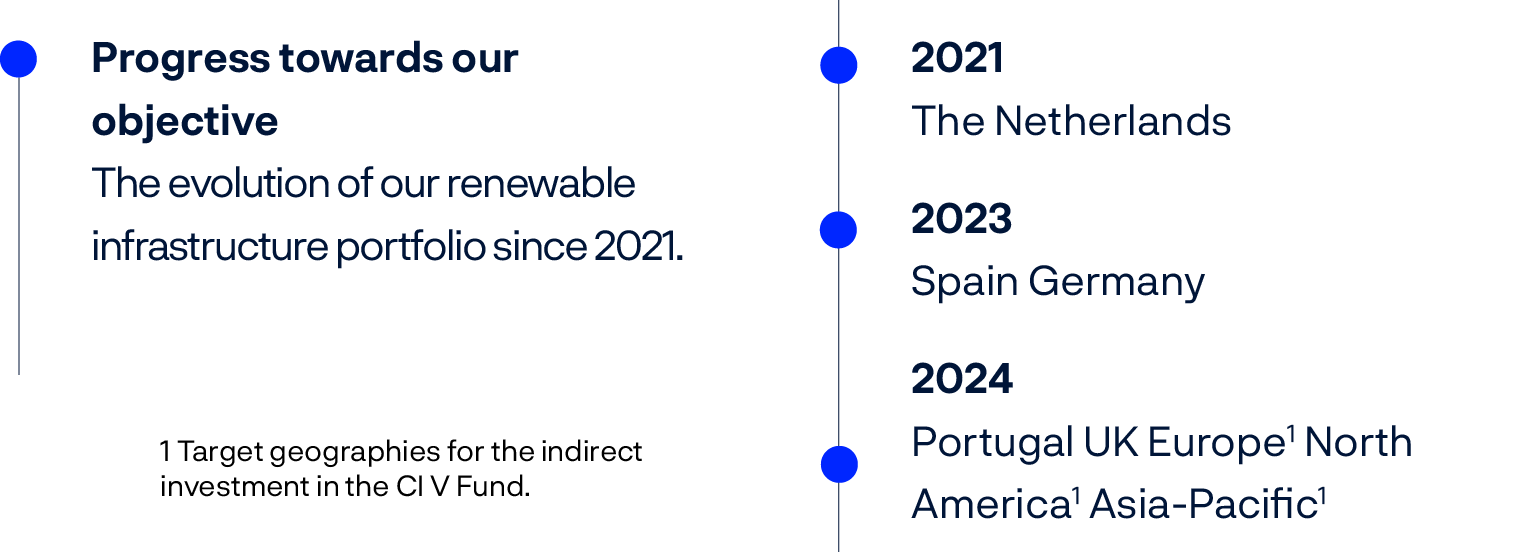

In 2024, we expanded our renewable energy portfolio and acquired stakes in both solar, onshore - and offshore wind projects, including joint ventures in Portugal and Spain and our first asset acquisition in the United Kingdom. We made our first indirect investment in wind, solar, and energy storage, enhancing the diversification and exposure to early-stage renewable projects across various regions.

1,891MV renewable electricity generation capacity added to the portfolio

Simpler, longer-term incentives in CEO pay

Simpler, longer-term incentives in CEO pay remain a priority for us, especially in the US. In 2024, we advocated for proxy advisors to solicit investors’ views on alternative pay models and are encouraged by policy changes. We hosted asset manager roundtables during two conferences of the Council of Institutional Investors to present our perspectives, worked with other stakeholders, and reiterated our opinion on the topic in Harvard Law School Forum. We discussed CEO pay with companies to better understand their approach and promoted our view. We opposed the largest CEO pay packages that we considered most misaligned with long-term value creation.

94 votes against relatively costly packages without an attractive time horizon

426 votes against CEO pay overall

9 academic projects

49 risk-based divestments

16 reversed risk- based divestments

Managing our risk-based divestments

Risk-based divestments are financially motivated decisions and part of our risk management. We may divest from a company if we assess that its long-term market valuation may be adversely affected by its mismanagement of social and environmental issues. Conversely, we may reverse risk-based divestments and make companies available for investment if we observe significant improvements.

Long-term value

Our task is to generate the highest possible financial return in a responsible manner. But what does it really mean to be a responsible investor?

The idea behind the Government Pension Fund Global is simple. We invest the income that Norway receives from the Norwegian oil and gas industry in international financial markets – in companies, government and corporate bonds, real estate and unlisted renewable infrastructure. As an investor in more than 8,500 companies across 70 countries, we own a small piece of the vast majority of publicly listed companies worldwide. The fund’s return stems from the value created in these companies. As long as one does not withdraw more from the fund than the expected return, the fund could, in principle, last forever.

In order for us to share in this value creation, we depend on companies that are responsible and long-term oriented. They must be able to operate in well-functioning markets and in a way that takes care of the world we live in. These are foundations that allow companies to exist and create value. Responsible investment supports the objective of the fund by furthering the long-term economic performance of our investments and reducing financial risks associated with the environmental, social and governance practices of companies in which we have invested.

Long-term growth is, at the same time, not something companies or investors alone can deliver. Even though we are among the largest owners in the world, we do not directly manage companies, and we do not decide on the business conditions they operate under. Being a responsible investor means doing what we can to ensure that the companies we own and the markets they operate in function as well as possible from an economic, environmental and societal perspective.

That is why the fund spends considerable time and resources on responsible investment. As an owner, we use our voice to engage with the companies and to exercise our voting rights at annual general meetings. We also work for market standards in support of well-functioning markets, good corporate governance and sustainable business models.

By doing so, our ambition is that companies and markets gradually move in the direction we believe is best for us as a long-term investor. Being a responsible investor is about contributing to value creation today, in ten years, fifty years and one hundred years.

Oslo, 6 February 2025

Nicolai Tangen

Chief Executive Officer

Beyond business as usual

Studies indicate that climate change poses a material risk to long-term value creation.

At Climate Week 2024 in New York, our message was clear: climate action is crucial for safeguarding financial returns. Our company engagements reinforce our conviction that this goes beyond “business as usual”.

In 2024, we engaged with companies on climate-related topics covering 54 percent of the fund’s financed emissions. The companies are responding. Companies responsible for 74 percent of the fund’s financed emissions now have net zero targets. Many companies view the energy transition as an opportunity, making substantial investments in clean technology and efficiency.

While this progress is encouraging, the transition must gather further pace, supported by coherent policy measures. And although we advocate for sustainable business transformation, we also recognise the significant challenges faced by many companies and respect their operational independence and need to adapt to their specific business environments. Guided by this approach, we support climate-related shareholder proposals relevant to value creation.

Board accountability is at the core of good corporate governance, also when it comes to companies’ management of climate risk. The boards must exercise oversight that support long-term value creation. They must strike a balance between short-term performance and long-term resilience. We expect boards to adopt credible net zero transition plans that are ambitious, but actionable.

As owners, we continuously seek to strengthen our interactions with portfolio companies. By combining company-specific investment insights, structured engagement tracking and progress assessments, we can refine our approach and improve our results. In 2024, we enhanced our ability to track and measure the progress of our ownership activities. It will help us identify where our engagement adds the most value and which strategies are most effective.

In this way we build more insightful and long-term relationships with companies. We believe that contributes to more sustainable business practices and higher value creation over time.

Oslo, 6 February 2025

Carine Smith Ihenacho

Chief Governance and Compliance Officer

How we work

We manage the fund according to a mandate from the Norwegian Ministry of Finance. The objective for the management of the fund is the highest possible return with acceptable risk.

Within the objective, our mandate requires us to manage the fund with high transparency and in line with internationally recognised principles and standards for responsible investing. The mandate also establishes that responsible investment activties shall be based on the long-term goal that the companies in the investment portfolio have activities that are compatible with global net zero emissions, in accordance with the Paris Agreement.

The fund’s long-term return is dependent on sustainable economic, environmental and social development, as well as well-functioning, legitimate and efficient markets. Through responsible investment, we seek to improve the financial performance of our investments and to reduce the financial risks associated with the environmental and social practices of companies in our portfolio. In line with international standards, we also carry out environmental and social due diligence and promote responsible business conduct. Our responsible investment work is directed at the market, portfolio and company level.

Market

Our goal is to contribute to well-functioning markets, good corporate governance and sustainable business models. We promote these economic interests in a predictable way through clear principles and public views. We also support academic research to improve the understanding of responsible investment.

Portfolio

Our goal is to integrate governance and sustainability considerations into investment decisions and assess companies’ ability to create value. This helps us manage risks and identify investment opportunities, including by investing in the transition to a low-carbon economy, or divesting where we believe high sustainability risks will adversely affect value creation.

Companies

Our goal is to promote value creation and reduce risk at the companies we invest in through active ownership. We do this through dialogue with companies and voting at their shareholder meetings. There are also companies we choose not to be invested in for ethical reasons. Where alleged conduct raises significant concerns about market integrity, we may consider legal action to protect our interests.

Standards

As a market participant in 70 countries, we benefit from well-functioning and legitimate markets, global solutions to common challenges, and generally agreed international standards.

Engaging with standard setters

We engage with relevant international organisations, standard setters and regulators to contribute to the development and adoption of standards on corporate governance, responsible business conduct and sustainability disclosures. We also participate in the development of best practices for responsible investment. We share our investor perspective with standard setters by responding to public consultations and meeting their experts. We also speak at conferences and take part in selected initiatives to reach a wider range of market participants. We do not engage with members of parliament or foreign governments, nor do we engage lobbyists or make political contributions.

Responding to consultations and meeting with regulators

In 2024, we saw an uptake in sustainability disclosure consultations, driven by the regulatory adoption of the International Sustainability Standards Board (ISSB) standards. We are particularly encouraged by the pace of adoption in the Asia-Pacific. We also observed reform in corporate governance requirements, driven by the aim to increase market attractiveness. In 2024, we responded to 30 public consultations on issues related to corporate reporting, corporate governance and climate risk. We submitted ten consultation responses to global standard setters, in addition to eight consultation responses in Asia, three in Europe, three in Australia and six in the Americas. We published our responses and held meetings with standard setters, securities regulators and stock exchanges and other relevant stakeholders.

- In Europe, the implementation of the Corporate Sustainability Reporting Directive (CSRD) is underway. We have for a long time highlighted the need for sustainability reporting standards that facilitate global interoperability and prevent double reporting. For this reason, we believe standards should be as aligned as possible with the global ISSB standards. In 2024, we argued for simplification and reduction in the data points included in the European Sustainability Reporting Standards (ESRS).

- Beyond Europe, we continued supporting the adoption of the ISSB standards by regulators and standard setters at jurisdictional level. We engaged in several listing rules reforms, such as in the United Kingdom, Hong Kong and Brazil, on the importance of corporate governance. At the global level, we contributed to the revision of the International Corporate Governance Network (ICGN) Global Stewardship Principles.

Strengthening our work in Asia-Pacific

Many markets in Asia-Pacific are reviewing their corporate governance and sustainability disclosure rules. Several jurisdictions have an ambitious agenda, focusing on improving equity valuations alongside sustainability and business resilience. Asia-Pacific’s role as a global supply chain hub makes the region an important one for our responsible investment work.

We have significant holdings in the Asia-Pacific region, with 19 percent of the fund invested in this market. The region represents over half of the world’s population and over a third of global trade. In 2024, we strengthened our engagement with regulators, stock exchanges, peer investors and companies in key Asia-Pacific markets to understand evolving market dynamics and share our views.

- In South Korea, we organised the Corporate Integrity Forum in collaboration with United Nations Global Compact Network Korea, to discuss anti-corruption, corporate governance and sustainability disclosures.

- In South Korea and Japan, we participated in investor delegations led by the Asian Corporate Governance Association to discuss corporate governance reform and its link to valuations.

- In China, we joined an investor study tour to exchange views on climate and nature risks, and global sustainability standards.

We benefit from industry initiatives to engage companies on common sustainability challenges and building capacity to address them.

- In Singapore, we hosted a workshop on financing the transition to more resilient agri-food systems. Companies and financial institutions shared their insights on value chain dynamics, best practices and solutions for advancing sustainable production.

- In Indonesia and Malaysia, we participated in a CITIC CLSA field trip to explore the environmental and social impacts of palm oil production, including site visits and meetings with plantation operators, smallholder farmers, NGO experts and industry bodies.

Through these engagements and initiatives, we deepen our market insights while contributing to improved corporate governance and sustainability standards.

Corporate governance reform and the attractiveness of listed markets

As an investor with around 70 percent of our holdings in listed equity, we need a thriving listed sector and public markets that reflect economic value creation. Different countries are taking diverging approaches to enhance their market attractiveness.

In 2024, the United Kingdom simplified its listing rules, allowing broader use of dual class shares and removing shareholder approval for related party transactions and significant deals. While intending to enhance London’s competitiveness, this strategy risks eroding investor confidence, potentially harming market integrity. We opposed these reforms in our consultation response.

Similarly, the EU facilitated multiple-vote shares to encourage listing by small and medium-sized enterprises. We advocated for EU-wide mandatory sunset clauses for enhanced voting rights, but the reform did not harmonise safeguard mechanisms. Meanwhile, Italy adopted legislation to enhance loyalty shares and Germany reintroduced multiple share class structures. While we acknowledge the importance of incentives to list, we consider these changes to be misaligned with equal treatment of shareholders.

Conversely, Brazil and Japan are working to strengthen their corporate governance standards. Brazil’s stock exchange B3 proposed stricter board composition and additional governance requirements for its Novo Mercado segment. Although we believe that B3 should move to majority independent boards, we welcomed the move closer to best practice. In 2023, the Tokyo Stock Exchange started addressing the cost of capital, aiming for higher valuations and corporate growth. Inspired by Japan, South Korea launched its own corporate governance reform to enhance capital efficiency and improve valuations.

The varied approaches to listing rules and corporate governance across these regions highlight the ongoing debate on how to attract new listings and foster market growth. We believe that robust corporate governance is key to support resilient public markets.

Participating in organisations and initiatives

International organisations and standard setters

We have long contributed to the development of principles for responsible investment and participate in various organisations and initiatives.

- Elected by asset owner signatories in 2021 and re-elected in 2024, we sit on the board of directors of Principles for Responsible Investment (PRI), of which we were a founding signatory in 2006. Our annual transparency report to PRI is available on PRI’s website.

- We have promoted the need for consistent and comparable sustainability disclosures for a number of years. In 2024, to further support these efforts, our Chief Governance and Compliance Officer was appointed chair of the ISSB Investor Advisory Group (IIAG). We also joined the Capital Markets Advisory Panel (CMAP) of the European Financial Reporting Advisory Group (EFRAG).

- We are a long-standing supporter of CDP and in 2024 we continued to provide a grant to support its work on ocean health and water security. We co-hosted a workshop with CDP at our offices in London with companies, investors, NGOs and academics to provide feedback on its ocean disclosure framework.

- We continued our membership in the Taskforce on Nature-related Financial Disclosures (TNFD), and participated in its Financial Institutions and Transition Planning working groups. In parallel, we continued advancing the application of the TNFD recommendations to our own portfolio. See our climate and nature disclosures for further information.

- We partnered in a symposium co-organised by the World Bank, the Green Climate Fund and Transparency International on integrity risks to climate finance and action, focusing on transparency and accountability as well as the challenges of existing anti-corruption mechanisms.

Working with other investors

To share our views, we may join investor coalitions or initiatives that are consistent with the fund’s mandate and support our management objective. However, we do not collaborate with other investors on investment decisions or voting at shareholder meetings, nor do we participate in coalitions that are primarily aimed at policy makers.

- On US CEO pay, we chaired a discussion at the Council of Institutional Investors conference, advocating for simpler and longer-term equity incentives. We explored the evolving opinions of US asset managers and proxy advisors. On the back of discussions with investors, both leading proxy advisors announced that they would implement changes. They will put more emphasis on longer-term stock lock-ins as a positive factor, and they will scrutinize ‘performance shares’ more closely. Institutional Shareholder Services (ISS), the proxy advisor with the largest market share, will consider whether to end its preference for performance shares versus simpler stock awards without performance metrics.

- On human rights, we serve as a co-lead investor in the PRI Advance stewardship initiative, engaging with a company in the mining sector. In 2024, our engagement focused on their asset-level operations and on freedom of association and human capital management. We also joined an investor initiative coordinated by the Church Commissioners for England, Aviva Investors and Scottish Widows, to improve data on corporate human rights commitments and due diligence processes.

- In real estate, we have been a steering committee member of Carbon Risk Real Estate Monitor (CRREM) since 2019. In 2024, we helped establish a new governance structure that will further develop CRREM as a global standard for decarbonisation pathways for operational emissions. We participate in Leaders of the Urban Future (LOTUF), an investor-led project to drive decarbonisation in real estate. In 2024, we hosted a summit in Berlin together with our investment partner Oxford Properties.

Building capacity with companies

We bring investors and companies together to discuss sustainability or governance challenges, consider solutions or share best practices. These capacity-building initiatives often focus on sector-specific or value chain challenges.

- On children’s rights, we collaborated with UNICEF to develop corporate disclosures on companies’ impact on children in the digital environment. In 2024, we conducted research on corporate disclosures in this area and facilitated a webinar to share the initial findings. We also organised a workshop in Geneva to gather feedback from companies, standard-setters, investors and civil society on the draft disclosures.

- On corporate policy engagement, we hosted a roundtable of experts, investors, and companies in New York to discuss oversight and transparency of such activities. We focussed particularly on climate policy engagement and the role of trade associations.

Engaging with our stakeholders

We value the ongoing dialogue we have with stakeholders. The information they share with us forms an important part of our responsible investment work, informing both our company engagements and our risk monitoring.

We regularly invite civil society to give us feedback on our responsible investment work. Each year, we organise seminars where civil society organisations can raise questions and provide input. In 2024, we organised seminars at our Oslo and London offices where we presented our work and received input on various topics. We also invite civil society to a presentation of our annual Responsible Investment report.

In 2024, civil society provided insights on topics such as indigenous peoples’ rights, climate lobbying, transition plans, risks in war- and conflict-affected areas, labour rights violations, and grievance mechanisms.

We communicate our work on responsible investment to the Norwegian people. We organise press conferences and participate in media interviews, and our Chief Governance and Compliance Officer writes regular op-eds in Norwegian news media. At Arendalsuka, an annual festival for open public discourse in Norway, we participated in events on topics such as financial risk in the energy transition, geopolitics, and AI. To strengthen the understanding of the fund’s role and build knowledge, we held 13 guest lectures at Norwegian and international universities on our approach to responsible investment. Our CEO’s podcast interviewing CEOs of companies we invest in reaches a broad audience.

Transparency about the management builds trust and knowledge about the fund, both in Norway and internationally. We disclose on our website increased information on our company engagements and their progress. In 2024, we received the ICGN Global Stewardship disclosure award, recognising our commitment to transparency and reporting. For the second year in a row, we were recognised as the world’s most transparent fund in the category on Responsible Investing by the Global Pension Transparency Benchmark.

Expectations

Starting from internationally agreed standards and informed by our dialogue with companies, academics and stakeholders, we set our own priorities as an investor. Our public positions on governance and expectations of companies on sustainability matters communicate our views to the wider market and ensure predictability for the companies we invest in.

Setting expectations of companies

Our expectation documents, covering ten key sustainability topics relevant to risk and return, form the basis of our dialogue with companies. They are primarily directed at company boards. We expect the board to take responsibility for company strategy and ensure that:

- Material sustainability risks and opportunities are integrated into the company’s strategy, risk management and reporting.

- The company’s adverse environmental and social impacts are understood and, to the extent possible, mitigated.

Our expectations and responsible investment management policy are based on standards such as the UN Global Compact, the OECD Guidelines for Multinational Enterprises, International Labour Organization (ILO) conventions and the UN Guiding Principles on Business and Human Rights. They also largely coincide with the UN Sustainable Development Goals.

In 2024, we updated our expectations on human rights providing additional detail on expectations of companies operating in conflict affected and high-risk areas, as well as stakeholder engagement and due diligence processes. We also updated our consumer interest expectation document to include the topic of animal welfare, reflecting emerging standards.

Communicating our positions and voting guidelines

To clarify our stance on corporate governance issues, we publish position papers. These are based on the G20/OECD Principles of Corporate Governance and best practices. We expect companies to have effective governance, and our rights as a shareholder to be protected. Our position papers are reflected in our global voting guidelines and affect how we vote at shareholder meetings.

In 2024, we strengthened our voting guidelines on board gender diversity, requiring at least two representatives of each gender in most developed markets, and at least one in most emerging markets.

Sharing our opinions on topical issues

We publish point-in-time opinions on topical issues that are relevant for us as investor. In 2024, we published our view on ESG ratings, responsible corporate policy engagement and global standards for corporate sustainability-related financial disclosures.

Corporate policy engagement

Corporate influence in policymaking has been a widely discussed topic for years. Businesses depend on effective, stable and predictable policy frameworks. Companies and the private sector play an important role in reaching a variety of policy objectives, not least those aimed at well-functioning markets, sustainability and long-term growth. We have an interest in how companies manage risks and opportunities in their policy engagement activities.

In 2024, we published our view on responsible corporate policy engagement. We are encouraged by the development of best practice principles in this area and the incorporation of policy influence into standards of responsible business conduct and corporate governance. This has improved oversight and transparency, but inconsistencies in practice and gaps in reporting remain. We communicated our view to companies, civil society, standard setters, and other investors, and organised a roundtable to facilitate further discussions. We also incorporated the topic of climate lobbying into selected company dialogues.

We consider key elements of responsible policy engagement to be:

Board oversight

Companies should establish strong governance mechanisms. Governance, due diligence and monitoring should be enhanced for indirect engagement via industry associations and other third parties.

Transparency

Transparency is essential to mitigate risk and maintain stakeholder trust. Comprehensive reporting of positions, activities, and expenditures is crucial for accountability.

Alignment between stated policies and policy influence activities

Companies should align their policy engagement activities with their publicly stated views and commitments, especially on material issues such as climate change.

Research

We aim to strengthen the scientific foundation of our responsible investment efforts. Academic research can help improve market standards, provide new data and inform our responsible investment with new insights.

We provide research funding in areas where we believe that more academic research is useful to shed light on how governance and sustainability affect financial risks and returns. Through targeted collaborations with academics, we investigate specific questions of relevance to our work while facilitating knowledge exchange between academia and the fund. We make the findings publicly available, contributing to knowledge building.

Supporting academic research

Climate finance

In 2024, we launched Call for Proposals in three areas of climate finance where we believe more academic research is necessary. Following the evaluation by Norges Bank’s Scientific Advisory Board, we decided to fund three projects.

Call for proposals topics

- Interactions between climate, nature, and financial risks

- Climate transition and geopolitics

- Climate action and its effectiveness

Selected projects

A project led by Imperial College in London, in collaboration with the University of Cambridge, aims to publish a Special Issue in the Review of Finance on Biodiversity Finance.

The National Bureau of Economic Research will organise three annual conferences, each to cover one of the key areas outlined in our Call for Proposals.

At New York University, Johannes Stroebel, Theresa Kuchler and Olivier Wang will conduct research on the measurement and management of nature risks and their pricing in financial markets.

Economics of natural resources

The interplay between climate change and natural resource availability may impact the fund in the long-term. In 2024, we continued to collaborate with Justin Johnson and Stephen Polasky at the University of Minnesota and the Natural Capital Project to analyse the long-term impacts of climate change and natural resource availability. Their model links climate, changes in resource availability, and their economic impacts on countries to shed light on how future supply and demand of natural resources may impact the fund’s equity investments.

Setting CEO incentives

Optimal executive incentives are important for a diversified investor seeking to promote long-term returns. In 2023, we signed an agreement with the National Bureau of Economic Research (NBER) to encourage further academic research on CEO incentives. In 2024, the NBER organised a doctoral training workshop on the economics of executive compensation in Cambridge, Massachusetts.

Ownership structure

Changing ownership structures, marked by a rise in institutional shareholders and their distinct preferences, could affect companies’ behaviour and decision-making. In 2024, two research projects approaching this trend from different angles came to an end.

- Research by the École Polytechnique Fédérale de Lausanne (EPFL) and the University of Zürich confirms that mutual funds by and large vote according to their proxy-voting guidelines. The researchers document evidence that portfolio companies and active investors monitor these guidelines. The findings align with the emerging academic consensus that passive investors oversight is most effective when exercised transparently and at scale such as through shareholder voting. The project was concluded with a conference at the University of Zürich.

- A project led by Martin Schmalz from the University of Oxford focused on laboratory experiments to examine the relationship between shareholders and boards. The results show that corporate managers take a holistic view and also consider the profits their shareholders can generate from their shareholdings in competing companies. The project concluded with a conference at Harvard Law School. Presentations showcased the growing body of research on board-shareholder dynamics, featuring both empirical studies across different investor types and asset classes, and theoretical contributions to the field.

Projects funded in 2024.

|

Institution |

Topic |

Project |

2024 payment. Dollar |

|---|---|---|---|

|

Imperial College in London and University of Cambridge |

Climate finance |

Biodiversity Finance Initative |

No payment in 2024 |

|

National Bureau of Economic Research |

Climate Finance |

||

|

The effects of climate change and biodiversity loss on the economy and financial markets |

|||

|

New York University |

|||

|

University of Minnesota |

Economics of natural resources |

Economics of natural resources under different climate scenarios |

No payment in 2024 |

|

National Bureau of Economic Research |

Setting CEO incentives |

Optimal executive incentives for investors |

263,000 |

|

École Polytechnique Fédérale de Lausanne & University of Zürich |

Ownership structure |

Evolution and determinants of institutional investor preferences |

No payment in 2024 |

|

University of Oxford |

Diversified institutional ownership and firms’ strategic behaviour |

26,000 |

Collaborating with researchers

Corporate perceptions of nature risk

In 2024, to better understand our portfolio companies’ perception of nature risk and the actions taken to address it, we started a project with Zacharias Sautner and Alexander Wagner from the University of Zürich. The research proposal has been accepted by the academic journal Review of Finance for potential inclusion in their planned Special Issue on Biodiversity Finance.

Effect of voting pre-disclosure

We want to learn more about the effectiveness of our ownership tools. An independent research study by Ruediger Fahlenbrach from EPFL, Nicolas Rudolf at HEC Lausanne and Alexis Wegerich from Norges Bank Investment Management, found that when we pre-disclose our intention to vote against a proposal, overall dissent appeared to increase by an average of 3 percentage points. A 2024 expansion of this research indicated longer-term impacts - companies experienced higher director turnover in the two years following elections where we opposed proposals.

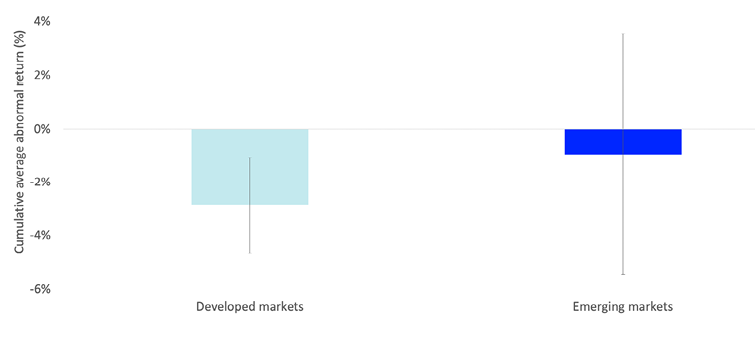

Research on stock price reaction to removing net zero targets

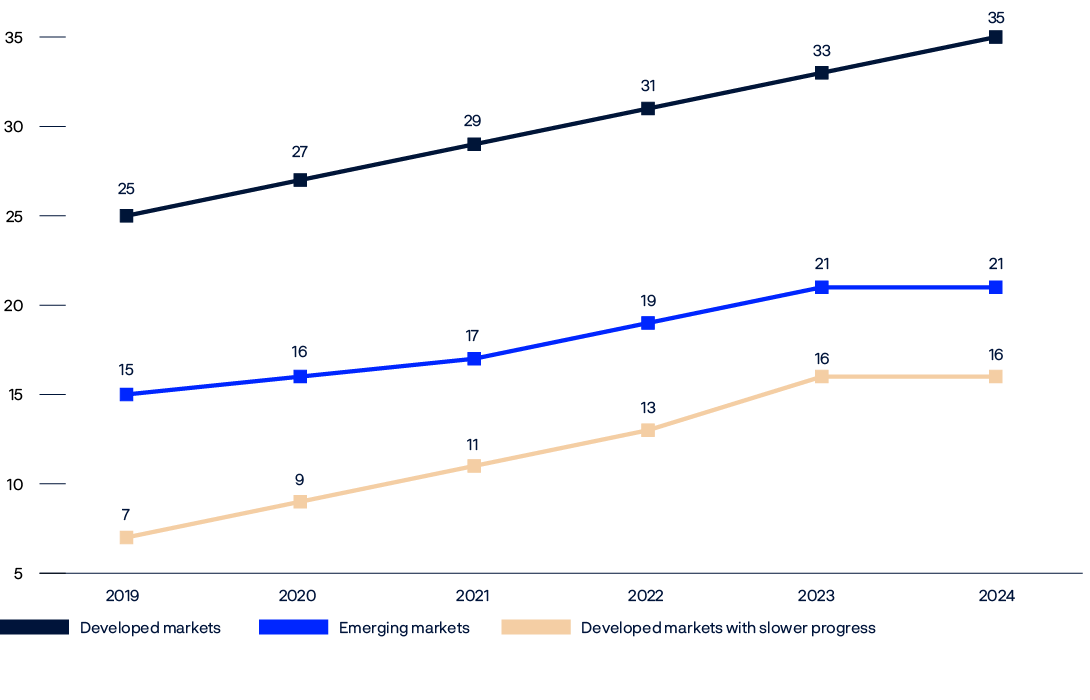

The aim of our 2025 Climate Action Plan is for our portfolio companies to achieve net zero emissions by 2050. At the end of 2024, 74 percent of financed scope 1 and 2 emissions were covered by net zero targets for 2050 or sooner, up 6 percentage points since 2023. Weighted by net asset value, the figure was 69 percent in 2024.

The Science Based Targets initiative (SBTi) defines standards for corporate net zero targets, and companies apply to the initiative to have their targets approved. We monitor companies’ progress in the SBTi target approval process, including which corporate targets are removed by the SBTi when companies fail to submit targets within the specified commitment period.

In 2024, we conducted an event study to examine stock price reactions to these removals. We found a significant negative stock market response, suggesting that investors are concerned with companies setting, but not following up on their climate targets. Such market reactions may also signal concerns about a company’s ability to execute on a credible transition plan. The negative returns following SBTi removal were more pronounced for companies in developed markets. For companies in emerging markets, the negative reaction appeared smaller and statistically insignificant.

Short-term share price reaction to removal of SBTi targets in 2024 – comparison between developed and emerging markets.

Note: This figure presents the cumulative average abnormal returns over an 11-day event window, spanning from t-5 to t+5 trading days, where t=0 represents the date of a firm’s status change to ‘Removed’ by the SBTi.

Investments

Governance and sustainability considerations are integrated into our investment processes across all asset classes. We believe this improves returns and reduces risk.

Investing sustainably

Integrating governance and sustainability into investment processes

Our management mandate has specific requirements for responsible investment. The quality of a company’s corporate governance, and the material sustainability risks and opportunities it faces, can impact its ability to create long-term value.

We believe that integrating governance and sustainability information is beneficial throughout the investment process and our portfolio managers are required to consider sustainability in their analyses. They are well-versed in our expectations on sustainability and positions on governance. They regularly discuss these with companies and collaborate closely with our investment stewardship managers. In 2024, they attended 2,610 meetings with companies, and in 60 percent of these they discussed governance and sustainability topics. Understanding the views of the company board or management improves the quality of our investment analysis and makes our responsible investment efforts more relevant. Over time, we believe this contributes positively to our investment performance.

In 2024, portfolio managers participated in voting decisions at 628 companies. These companies are among our largest investments and together made up 63 percent of the equity portfolio’s market value.

Benefiting from long-term company relationships

We have been investing in equities for more than 25 years. Due to our size and investment mandate, we tend to be among a listed company’s larger shareholders over time. The fund’s long investment horizon underpins our responsible investment approach. It enables us to invest and engage with companies beyond the scope of many other investors. Our permanence of capital and size also provide good access to companies.

In 2024, we gathered internal experts to recommend ways in which we can benefit further from our investment horizon. They emphasised the value of consistent, two-way dialogue in building enduring relationships with companies, relying on a deep understanding of each company and its sector.

The participants recommended more knowledge sharing and training on managing company relationships and identified opportunities to enhance our communication on voting. Another recommendation was to examine how we can encourage long-term thinking and decision making in the companies we invest, including through company reporting frequency.

Building responsible investment knowledge

We foster a responsible investment mindset across the organisation, offering employees training on important governance and sustainability topics:

- During our inaugural internal investment summit, we gathered speakers from the international investment community, external fund managers and our own investment teams. Across workshops and lectures, participants emphasised the value of robust governance and high management quality, and shared best practices for how to further integrate these elements of corporate governance in the investment process.

- We regularly hold learning sessions for our employees, inviting external speakers from academia and industry to talk to us about governance and sustainability-related developments. As an example, we invited a company board representative to share perspectives on shareholder engagement from the board.

- We included several lectures on responsible investment in our internal Investment Academy training programme. We covered topics related to our active ownership approach, climate risk and renewable energy infrastructure. We also provided training on the current geopolitical landscape, linking it to topics such as renewable infrastructure, climate change, global energy systems and energy transition.

Enhancing data and tools in the investment process

We make a broad set of company specific governance and sustainability information available to the organisation in our research and portfolio management systems. We continuously develop these tools and made several new features available during 2024:

- We added a regulatory monitoring feature that allows portfolio managers and others in the organisation to review governance and sustainability- related policy developments that are relevant to a specific company or sector.

- We enhanced our internal model for analysing governance and sustainability risks across companies based on the markets and sectors they operate in.

- We expanded our climate performance feature by adding information on companies’ carbon emissions performance relative to peers, the ambition level and quality of their net zero targets.

- We systematically conduct analyses of earnings calls or financial statements to identify potential red flags. These signals are integrated in our investment tool and flagged to portfolio managers when assessing a company to invest in or when they place a trade.

- We developed a screening tool which examines the movements of senior personnel involved in companies where there have been major concerns about fraud, and flags whether they have moved into other companies in our portfolio.

- We deployed AI models to systematically analyse earnings call transcripts and identify how companies discuss climate-related topics. These models accurately recognise trends even when companies use varying terminology.

Expectation scores

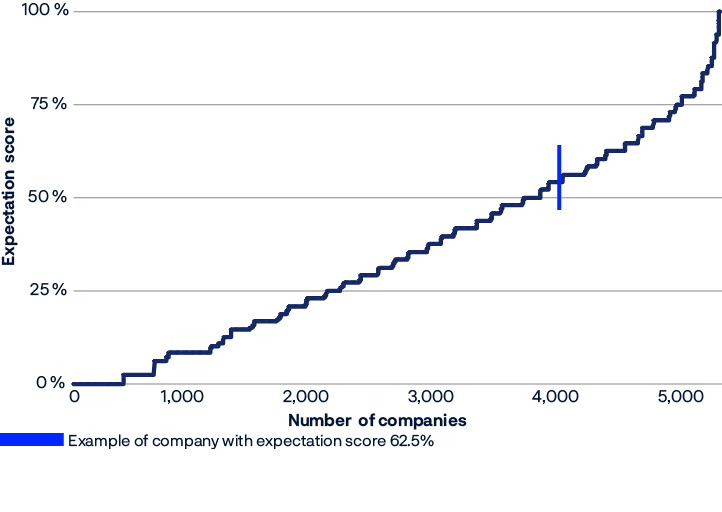

We want to see how our portfolio companies are progressing on their governance and sustainability practices, to better inform our investment and ownership decisions.

In 2024, we enhanced our assessments and introduced expectation scores, a systematic evaluation of companies’ disclosures against our sustainability expectations. In addition to leveraging data from multiple data providers, we use AI to extract sustainability data from public disclosures that are specific to our needs and not readily available in the market. We also use machine learning techniques to handle missing data, supporting robust and complete evaluations.

The scores assess companies’ performance on key expectations such as climate risk management, anti-corruption measures, biodiversity impact assessments, and human rights policies. Although data availability varies between different sustainability topics, our coverage is extensive – the scores are available for several thousand companies, representing approximately 90 percent of our portfolio by net asset value.

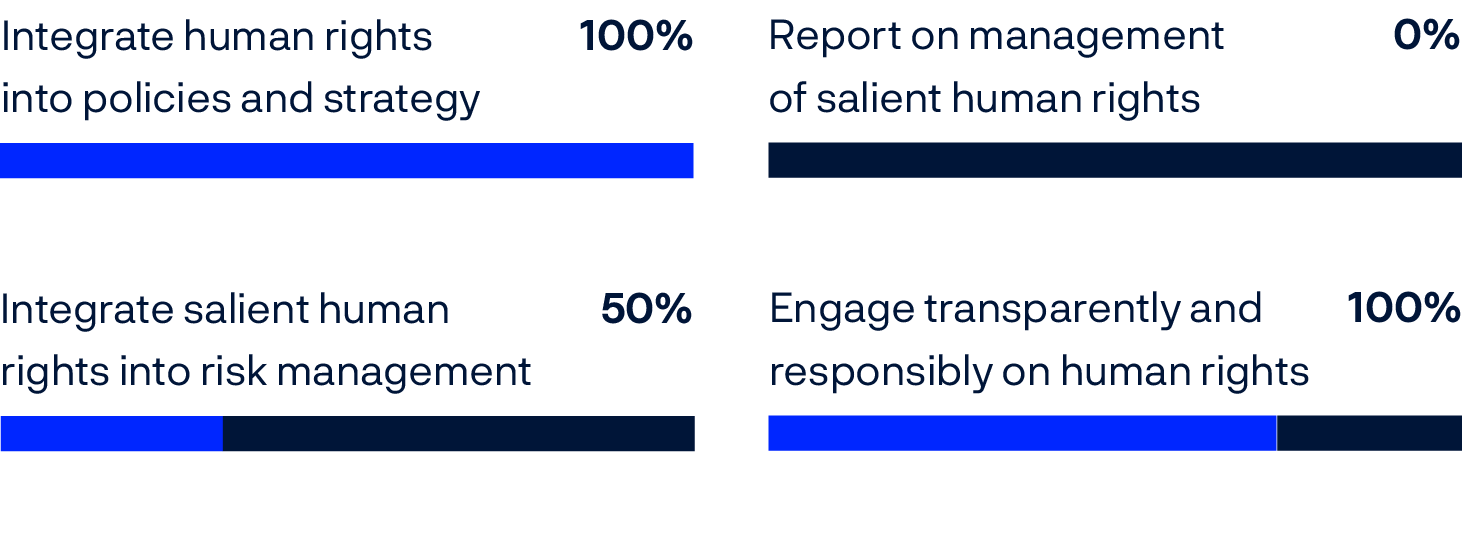

This approach allows us to identify the strongest and the weakest performers on different criteria, enabling targeted engagement from our investment and stewardship teams. As an example, we scored 5,177 portfolio companies against our expectations on human rights. The figure below shows the distribution of scores and provides an example of a company’s results.

Expectation score on human rights.

The fund and the energy transition

The fund has significant investments in companies supporting industrial decarbonisation, and in companies involved in the energy transition.

Our Climate Advisory Board is supporting us in the implementation of our 2025 Climate Action Plan. The external members, Professor Jody Freeman, Jennifer Morris, Huw van Steenis and Bjørn Otto Sverdrup have extensive knowledge in climate risk, market standards and finance. In 2024, we had three meetings with the Board and received advice on topics including companies’ decarbonisation investments, trends in climate investing among financial institutions, and the relevance of nature risk for our climate work.

Share of our equity portfolio invested in companies supporting industrial decarbonisation and involved in the energy transition in 2024.

Achieving a net zero global economy by 2050 presents major challenges, with primary energy demand potentially doubling, if current growth rates continue. Meeting this demand requires a sixfold increase in renewable energy production within three decades, even if fossil fuel consumption remains at today’s high, environmentally unsustainable levels.

For our portfolio companies, this context highlights significant risks and opportunities. Regulatory changes, stranded assets and fossil fuel volatility threaten returns. Conversely, renewable energy infrastructure expansion and investments in companies leading in low-carbon innovation provide growth opportunities.

Our 2025 Climate action plan sets out our intention to increase our investments in renewable energy infrastructure and dedicate investment mandates to opportunities in the low-carbon transition.

In 2024, we established an energy investment department to explore new investment opportunities in the listed and unlisted market for renewable energy infrastructure and capitalise further on existing relationships with companies.

Our long-term investment horizon and strong liquidity position allow us to act differently from other market participants, particularly in volatile and illiquid markets. In addition, our size grants us economies of scale, enabling cost-effective implementation of new investment strategies. This scale also grants us access to company management and investment opportunities, including in unlisted markets.

Investing in renewable energy infrastructure

Up to 2 percent of the fund can be invested in unlisted renewable energy infrastructure. At the end of 2024, these investments represented 0.1 percent of the fund. These are active investment decisions and investments in this asset class are subject to the same risk and return requirements as the fund’s other investments. Each investment is also subject to a thorough due diligence review including assessments of risk factors relating to health, safety, environment, corporate governance and social considerations.

In 2024, we expanded our renewable energy portfolio through several strategic investments, including joint ventures in Portugal and Spain, our first asset acquisition in the United Kingdom and a commitment to the Copenhagen Infrastructure V (CI V) fund with Copenhagen Infrastructure Partners (CIP), which enhances diversification and exposure to early-stage renewable projects across various regions.

Renewable energy infrastructure investments in 2024.

|

Month |

Partner |

Stake |

Type |

Location |

Capacity |

Impact |

|---|---|---|---|---|---|---|

|

January |

Iberdrola |

49% |

Solar and onshore wind |

Spain and Portugal |

674 MW |

Powers equivalent of 350,000 Spanish households |

|

April |

Iberdrola |

49% |

Solar |

Spain |

644 MW |

Powers equivalent of 400,000 Spanish households |

|

June |

Arjun Infrastructure Partners and Ørsted |

37.5% |

Offshore wind |

UK |

573 MW |

Powers equivalent of 510,000 UK households |

|

August |

Copenhagen Infrastructure Partners: CI V Fund |

Anchor investor |

Indirect investment in wind, solar, and energy storage |

Europe, North America, Asia-Pacific |

N/A |

Expands exposure to early-stage projects and segments of the energy value chain |

Case study: Expanding our renewable energy infrastructure portfolio

Objective

Strategic growth of the renewable infrastructure portfolio.

Our approach

We are gradually building a portfolio of renewable infrastructure assets.

Our investment strategy is centred around acquiring high-quality assets that offer sustainable, long-term returns. We emphasise diversification across both renewable energy technologies and geographical regions. This approach helps us spread the risk, while leveraging new developments in different renewable energy sectors.

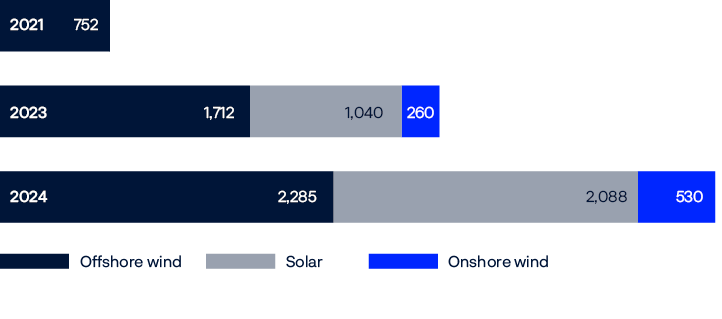

Installed capacity per energy sector. Megawatt.

Solar energy in the Iberian Peninsula – an example of our approach

Solar energy drives the global energy transition by providing a clean, renewable energy, while reducing fossil fuels dependency and greenhouse gas emissions. Our collaboration with Iberdrola on a 644 MW solar energy portfolio in Spain exemplifies our approach. The portfolio includes two solar plant projects: one plant is already operational, while the development of the second is expected to be completed by 2025. Our investment approach is aimed to mitigate power price risk and achieve stable revenues. This investment provides us exposure to the growing solar sector in the Iberian Peninsula.

Improving risk and return with external managers

External managers play an important part in the fund’s management. We use external managers to manage parts of the fund’s equity investments, primarily in emerging markets and small-cap companies in developed markets. Their proximity to the markets and expertise in specific regions and sectors help mitigate investment risk and enhance return. The fund had 982 billion kroner, or 5.0 percent of its capital, invested with external managers at the end of 2024.

We conduct annual due diligence on our external managers, assessing their integration of governance and sustainability factors and communicating our expectations. This process shows that our external managers actively engage with company management on governance and sustainability issues, and that they integrate governance and sustainability considerations into their stock screening and monitoring processes.

We have seen examples of how they promote board independence, executive remuneration in line with shareholder interests, as well as how they monitor the greenhouse gas emissions of high-emitting companies. In energy-intensive sectors, they track renewable energy adoption and targets for alternative fuel usage. When investing in chemical and hydropower companies, they focus on water usage and mitigation of operational sustainability risks.

In 2023, 60 percent of our external managers were signatories to the PRI.

Investing sustainably in fixed income

Poor corporate governance or high sustainability risks can become a significant credit risk and impact returns. We use internal knowledge and external sources to understand these risks - both before investing and on an ongoing basis.

We invest in green, social and other labelled bonds, but do not have a specific mandate related to these instruments. This means that we assess all bonds, conventional or labelled, in the same manner. Our view is that labelled bonds should adhere, at a minimum, to the International Capital Market Association’s principles.

We own labelled bonds issued by public entities, including sovereign, supranational and agency issuers, and the private sector. Most of these labelled bonds are green bonds, a type of fixed-income instrument that is specifically aimed at raising money for climate and environmental projects. These can include projects related to renewable energy, energy efficiency, green transport, biodiversity conservation, and other related sustainable and eco-friendly projects.

At the end of 2024, green bonds in the fixed-income portfolio amounted to 108 billion kroner, based on the definition for the Bloomberg Barclays MSCI Green Bond Index.

Net zero transition in unlisted real estate

Unlisted real estate investments amounted to 1.8 percent of the fund’s net asset value at the end of 2024. We invest in office and retail properties in selected cities around the world and in logistics properties that are part of global distribution networks.

Our 2050 net zero target cover emissions from the full life cycle of the buildings we own. These emissions include operational carbon required to operate the building (all landlord and tenant spaces) and embodied carbon required to construct, renovate, and demolish the building.

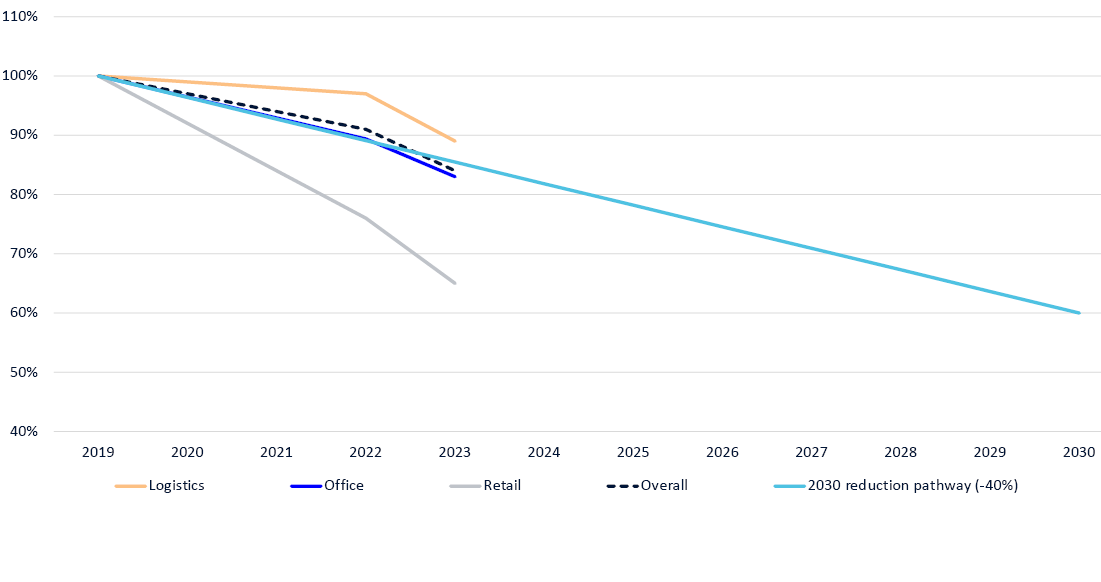

To measure progress towards net zero, we have set an interim target to reduce carbon emission intensity by 40 percent by 2030. We measure reduction in carbon emission intensity against a 2019 baseline. From 2019 to 2023, the real estate portfolio’s carbon emission intensity fell by 16 percent.

There are several factors that impact the carbon emission intensity of our portfolio, and the decarbonisation trajectories can vary greatly between real estate sectors. We work to improve the buildings we own. This is financially motivated, we will not divest energy intensive real estate sectors solely to meet our carbon emission reduction targets. We break down emission reductions by sector and disclose contributions by sector and geography to be transparent about our progress. See our 2024 Climate and nature disclosure for further information.

Progress towards 2030 interim target, carbon emission intensity by sector relative to 2019 baseline and 40 percent carbon emission reduction pathway.

We prefer actual energy consumption data over estimated consumption for each building when developing net zero transition plans for our portfolio. In 2023, we increased our consumption data coverage from 62 percent in 2022 to 71 percent of the properties’ gross asset value. This increase was driven by significant efforts by our joint venture partner, Prologis, to enhance its data strategy and improve quantity and quality of consumption data. We are still unable to analyse the Central London joint venture portfolio with The Crown Estate but continued to engage with our partner as they worked to improve their data coverage.

Where we have actual energy consumption data, we benchmark our unlisted real estate portfolio against 1.5°C decarbonisation pathways developed by Carbon Risk Real Estate Monitor (CRREM). CRREM assesses whether our portfolio’s current and projected emissions align with the global climate targets in the Paris Agreement. This assessment helps us understand the potential financial and operational risks associated with our buildings’ emissions in a low-carbon future.

The result of the CRREM analysis formed an integral part of a strategic emission review of our real estate portfolio that we completed in 2024. We detected outliers by identifying buildings in the top quartile of emissions in their respective regions and where their emissions intensity was above the CRREM emissions intensity decarbonisation pathway for 2030. We then conducted workshops with the investment teams to optimise the prioritisation of energy retrofits in the coming years.

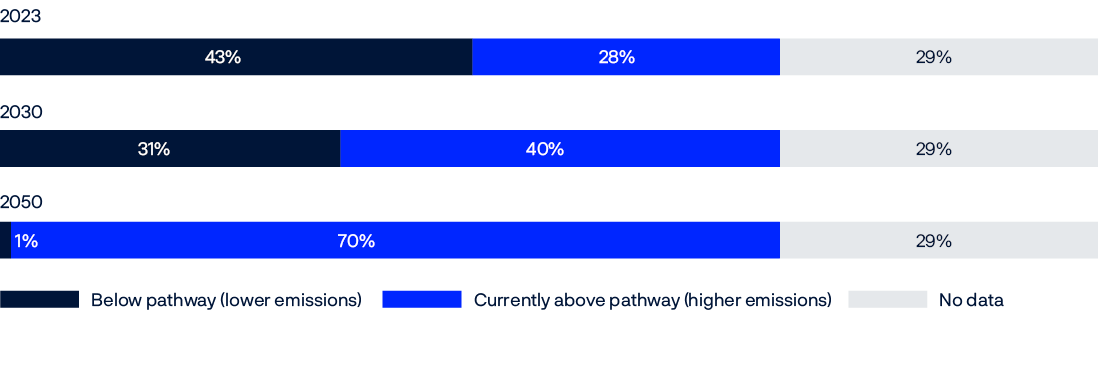

43 percent of the unlisted real estate portfolio by value was aligned with the 2023 value of the CRREM decarbonisation pathway compared with 41 percent in 2022. In the absence of further improvements, 31 percent of the portfolio is projected to be aligned with the pathway by 2030. This percentage will increase as we implement planned interventions across the portfolio over time.

Unlisted real estate portfolio alignment (current and projected) with CRREM decarbonisation pathway. Measured in kroner. Percentage points.

Risk management

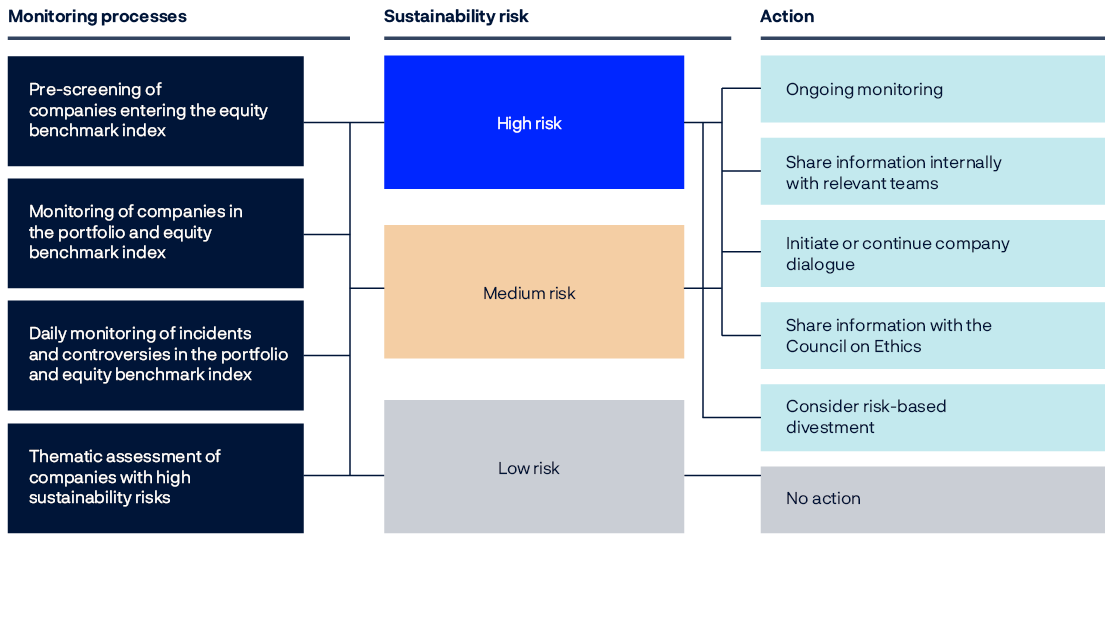

We monitor sustainability risks in the portfolio. We implement risk mitigation measures for companies with high risks, including company engagement, knowledge-sharing and divestment.

We monitor sustainability risks across all companies in the equity portfolio and equity benchmark index. In broad terms, we consider sustainability risk to be high if we believe a company’s long-term market valuation could be adversely affected by its mismanagement of social and environmental issues. We also seek to identify potential and actual impacts that companies may have on the environment and society.

We have established several systematic risk monitoring processes that help us identify sustainability risk. Our assessments are informed by a variety of information sources, such as corporate disclosures, data from external providers, the media and other public information. In areas where we have data gaps, we may use estimates.

Overview of our sustainability risk monitoring processes

We have built a country-sector risk model that helps us assess sustainability risk across all companies in the portfolio and in the benchmark index. It is based on the premise that a company’s main market and sector can be indicative of the environmental and social challenges it faces. The model includes all sustainability topics covered by our expectation documents and the risk metrics for each sector are aligned with SASB ‘s financial materiality framework. We use the model as a first layer of analysis for monitoring sustainability risk across our markets.

Norges Bank’s Executive Board is responsible for approving all the markets and sovereign bond issuers the fund invests in. The approval of new markets is based on a full assessment of market risk and considers political, regulatory and sustainability factors.

We may take several actions to manage the fund’s exposure to sustainability risks. Which action we take depends both on the level of sustainability risks identified through our monitoring processes and on the characteristics of our investment, including the size and history of the investment, its benchmark weight, and our relationship with the company.

Pre-screening of companies entering the equity benchmark index

The fund’s investment strategy is based on spreading our investments globally in accordance with a global market-weighted index. The selection of companies in the index and their relative index weights are adjusted every quarter by FTSE, our index provider, to reflect changes in the equity market. Given our mandate, we are expected to invest in most companies that enter the index. FTSE announces which companies will enter its global index four weeks in advance of their inclusion. Since 2021, we have as-sessed sustainability risk at all companies that FTSE has added to its global index. Pre-screening allows us to systematically assess the sustainability risks of potential investments before they enter our index.

|

Number of companies |

2024 |

|---|---|

|

Pre-screened |

533 |

|

Identified with high exposure to sustainability risks |

123 |

|

Placed on ongoing monitoring list |

70 |

|

Decided to divest from, or abstain from investing in |

27 |

Monitoring of companies in the portfolio and equity benchmark index

We assess the sustainability risk associated with all companies in the portfolio every quarter and initiate risk mitigation actions for all high-risk companies. We assess the potential financial impacts that sustainability risks may have on companies, as well as the companies’ potential and actual adverse impacts on the environment and society. We also consider how companies manage risks based on our expectation documents. This quarterly monitoring feeds into our sustainability due diligence processes. In addition, we monitor changes in our benchmark index and portfolio and corporate events that can result in heightened sustainability risks. For instance, we assess the sustainability risk profile of companies in which our ownership share exceeds 5 percent, making the fund a significant owner.

|

Number of companies |

2024 |

|---|---|

|

Identified with high exposure to sustainability risks |

265 |

|

Placed on ongoing monitoring list |

218 |

|

Initiated dialogue with |

10 |

|

Continued dialogue with |

33 |

|

Decided to divest from, or abstain from investing |

4 |

Daily monitoring of incidents and controversies in the portfolio and equity benchmark index

We monitor news flows on sustainability -related incidents and controversies in our portfolio on a daily basis. This allows us to identify emerging sustainability trends that impact the companies in which we are invested. It also provides insights into how their business conduct impacts the environment and society in the markets where they operate. Examples include environmental accidents, labour relations, corruption charges, lawsuits related to consumer rights, or government investigations of various kinds.

|

Number of companies |

2024 |

|---|---|

|

Identified with high exposure to sustainability risks |

111 |

|

Decided to follow up through other internal processes |

90 |

|

Decided to divest from |

12 |

Thematic assessments of companies with high sustainability risks

We may conduct deeper research into particular themes or trends where we see heightened sustainability risks. Similarly, we may re-assess previous decisions to divest from companies with high sustainability risk. In 2024, we looked at themes related to human rights, climate risk, tax and transparency, poor water management.

|

Number of companies |

2024 |

|---|---|

|

Decided to divest from |

6 |

|

Decided to reverse previous divestment decision |

16 |

Risk-based divestments

Risk-based divestments are financial decisions. When we divest from a company, we sell our holdings and stop making new investments. The tool is used for relatively small investments where other actions are deemed inappropriate. If circumstances change, we can decide to reverse the risk-based divestment and make companies available for investment.

Risk-based divestments are made within the parameters of the fund’s management mandate. Divested companies remain in the equity benchmark index and impact the fund’s relative returns. The divestment decisions are not made public, in line with the fund’s investment decisions. In contrast, companies excluded from the fund by the Executive Board on the basis of recommendations from the Council on Ethics, are removed from the benchmark index and therefore do not impact the fund’s relative return. These ethical exclusions are not financially motivated decisions and are disclosed publicly.

Risk-based divestments are investment decisions, which are not considered by the Executive Board. It is typically a tool for smaller investments where we have uncovered systematic mismanagement of governance and sustainability risks, and where engaging with the company has failed or is unlikely to succeed. In practice, divestment means that companies are removed from the investment universe of our portfolio managers and are no longer investable. We may also also reverse previous divestment decisions if our analysis finds that the they have shown improvements.

Risk-based divestments

In 2024, we divested from 49 companies. Of these, 27 decisions involved companies that entered the fund’s benchmark index during the year. We identified companies with significantly heightened risks across a variety of sustainability topics, including potential violations of human and labour rights, insufficient management of corruption risk, and business models highly exposed to environmental risk. Altogether, we have made 575 divestment decisions since 2012.

Reversed risk-based divestments

We made our first divestment decisions in 2012. Circumstances can change since we made the decision to divest. Companies may become more sustainable by changing their business models and practices. If we observe a positive change and conclude that companies no longer pose a long-term risk to the fund, we may reverse the divestment decision.

In 2024, we re-assessed a set of divested companies in the industrials and basic materials sectors that were initially divested on the grounds of high greenhouse gas emissions, poor water management and risks related to deforestation and tax issues. We reversed 16 risk-based divestments and made them available for investment. Altogether, we have reversed 25 risk-based divestments since 2012.

When divested companies improve their sustainability practices

In 2014-2015, we divested from three Asian industrial companies due to high greenhouse gas emissions and lack of emission reduction targets. By 2024, these companies were disclosing their emissions, had set net zero targets, and had reduced emissions.

In 2015-2016, we divested from four Asia-Pacific mining companies due to poor water management and conflicts with local communities. By 2024, these companies had shown signs of improvements in both areas.

Between 2021 and 2024, we divested from 17 companies due to high tax risk and inadequate tax management. By 2024, four of these had improved their tax disclosures and practices and and their tax risk appeared reduced.

We made the companies available for investments again.

Risk-based divestments in 2024.

|

Topic |

Criteria |

Divestments |

Reversed divestments |

|---|---|---|---|

|

Climate change |

Responsible for high green house gas emissions, including coal mining and coal-based electricity generation |

5 |

3 |

|

Water management |

Insufficient risk management related to water use |

3 |

4 |

|

Biodiversity and ecosystems |

Exposure to markets associated with degradation of biodiversity and ecosystems |

2 |

1* |

|

Anti-corruption |

Exposure to markets with significant risk of corruption |

8 |

2 |

|

Insufficient risk management related to corruption and corporate governance |

|||

|

Tax and transparency |

Elevated risk of aggressive tax planning |

0 |

4 |

|

Human rights |

Exposure to markets with significant risk of violations of human rights violations |

15 |

2 |

|

Insufficient risk management related to human rights |

|||

|

Human capital management |

Exposure to markets with significant risks related to human capital management |

5 |

|

|

Insufficient risk management related to human capital management |

|||

|

Consumer interests |

Insufficient risk management related to consumer interests |

3 |

|

|

Other |

Exposure to other significant sustainability risks |

8 |

*The reversed divestment relates to a company that was divested in 2019 under the climate change criteria, and where the underlying reason was due to deforestation. The expectation document on ‘Biodiversity and Ecosystems’ was issued in 2021.

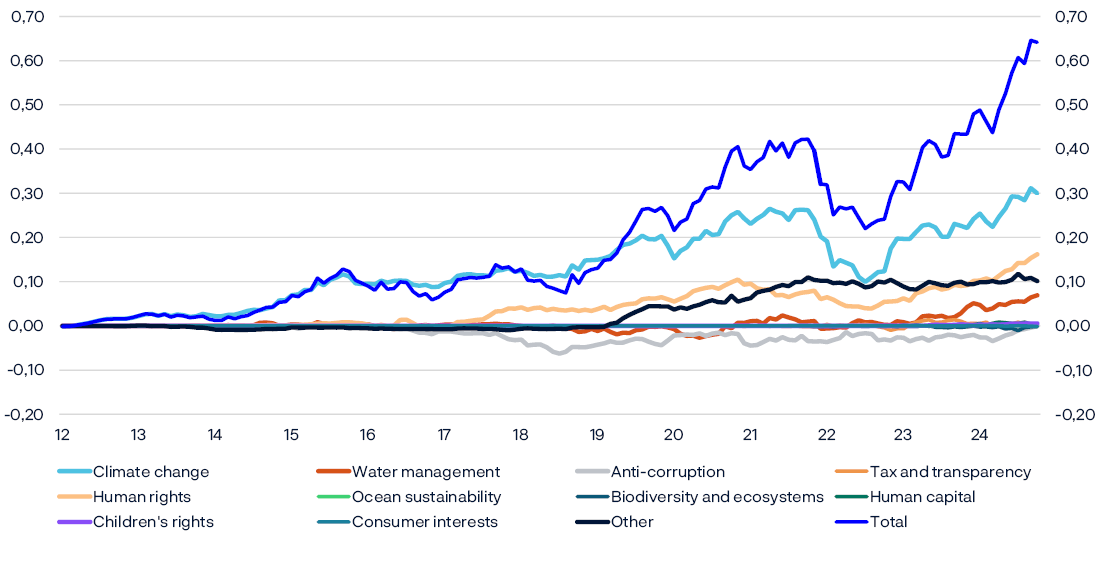

Impact on the fund’s equity returns

We measure the impact of our investment decisions, including risk-based divestments, on our returns. The impact on the equity portfolio from risk-based divestments was 0.05 percentage point in 2024.

Since 2012, risk-based divestments have increased the cumulative return on equity management by 0.64 percentage point, or 0.02 percentage points annually. Risk-based divestments linked to climate change and human rights have increased the cumulative return on equity management by 0.30 and 0.16 percentage point respectively.

Return impact of risk-based divestments on the equity reference portfolio, compared to a portfolio not adjusted for risk-based divestments. Measured in dollars. Percentage points.

Contribution to return impact of risk-based divestments on the equity reference portfolio as at 31 December 2024. Market value in billions of kroner. Contribution measured in dollars. Percentage points.

|

Expectation |

Number of companies divested1 |

Market value in the reference portfolio if not sold |

2024 |

2012–2024 annualised |

|---|---|---|---|---|

|

Climate change |

195 |

20 |

0.02 |

0.01 |

|

Water management |

61 |

3 |

0.01 |

0.00 |

|

Biodiversity and ecosystems |

16 |

2 |

0.00 |

0.00 |

|

Ocean sustainability |

3 |

0 |

0.00 |

0.00 |

|

Anti-corruption |

53 |

7 |

0.01 |

0.00 |

|

Tax and transparency |

17 |

5 |

0.00 |

0.00 |

|

Human rights |

135 |

13 |

0.02 |

0.00 |

|

Human capital |

24 |

2 |

0.00 |

0.00 |

|

Children’s rights |

3 |

1 |

0.00 |

0.00 |

|

Consumer interests |

5 |

1 |

0.00 |

0.00 |

|

Other |

63 |

6 |

-0.01 |

0.00 |

|

Total |

575 |

60 |

0.05 |

0.02 |

1 Includes companies that are not in the reference portfolio.

Dialogue

We engage in regular dialogue with our portfolio companies to promote good corporate governance, sustainable business models and responsible business practices. Our company meetings are conducted by our investment and active ownership teams and aim to contribute to reduced risks and improved value creation at companies.

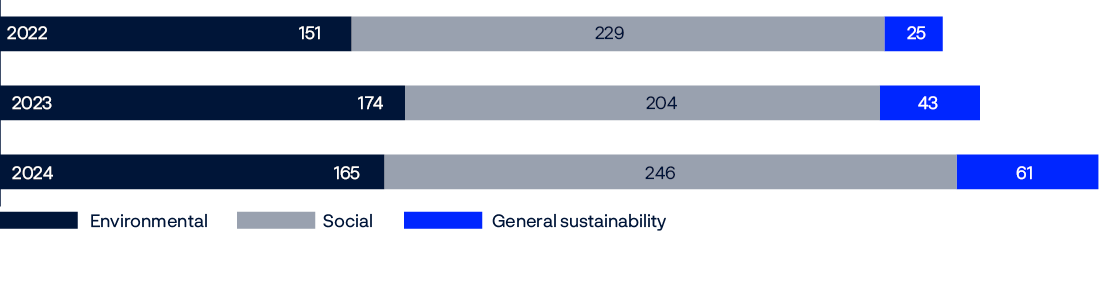

As a shareholder in more than 8,500 companies, we need to prioritise our company dialogues. We are in regular dialogue with our largest investments. In 2024, we held a total of 3,313 meetings with 1,342 companies. We discuss a broad range of strategic topics, such as performance, market developments, corporate governance and sustainability. The meetings can be with companies’ board and top management, business unit leaders, investor relations and/or sustainability experts.

Our dialogues take various forms, depending on whether we want to discuss specific issues or have a more wide-ranging discussion:

- Regular dialogues

- Strategic board dialogues

- Net zero dialogues

- Thematic dialogues

- Incident-based dialogues

- Dialogues about ethical criteria

Regular dialogues are the largest category of our company meetings. Companies often reach out to us as part of their annual shareholder interaction, or ahead of their annual shareholder meeting, to discuss executive remuneration or other items submitted for shareholder approval.

Alongside meetings, we communicate with companies in writing. We distribute our expectation documents and position papers to companies to inform them of our priorities, and respond to enquiries from companies.

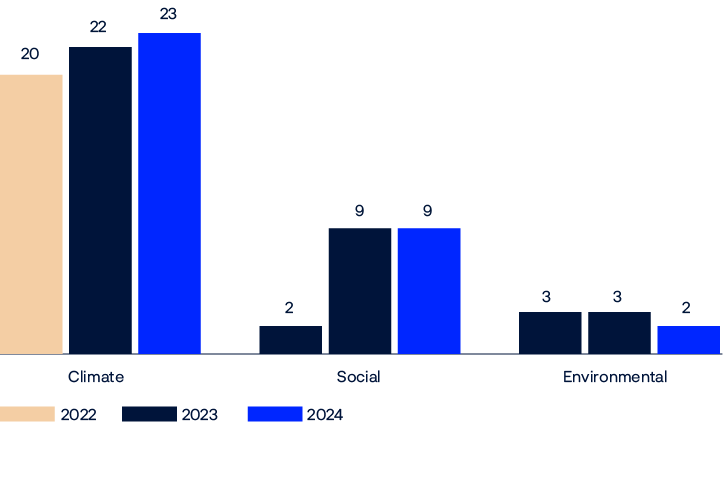

Overall, we held 1,986 meetings with 950 companies in 2024 where governance and sustainability topics were discussed, covering 60 percent of our company meetings and 65 percent of the value of the equity portfolio.

Number of company meetings where governance and sustainability topics were discussed.

|

Category |

Topic |

Number of meetings |

Share of equity portfolio in percent |

|---|---|---|---|

|

Environment |

Climate change |

727 |

31 |

|

Circular economy |

137 |

6 |

|

|

Biodiversity |

51 |

2 |

|

|

Water management |

53 |

2 |

|

|

Deforestation |

31 |

1 |

|

|

Ocean sustainability |

6 |

0,2 |

|

|

Other environmental topics |

233 |

8 |

|

|

Social |

Human capital |

492 |

22 |

|

Consumer interests |

157 |

20 |

|

|

Human rights |

111 |

20 |

|

|

Tax and transparency |

86 |

3 |

|

|

Data privacy |

25 |

12 |

|

|

Anti-corruption |

46 |

5 |

|

|

Children's rights |

17 |

5 |

|

|

Other social topics |

234 |

14 |

|

|

Governance |

Capital management |

1161 |

39 |

|

Effective boards |

337 |

37 |

|

|

Remuneration |

277 |

33 |

|

|

Enhanced reporting |

113 |

5 |

|

|

Protection of shareholders |

105 |

13 |

|

|

Other governance topics |

381 |

26 |

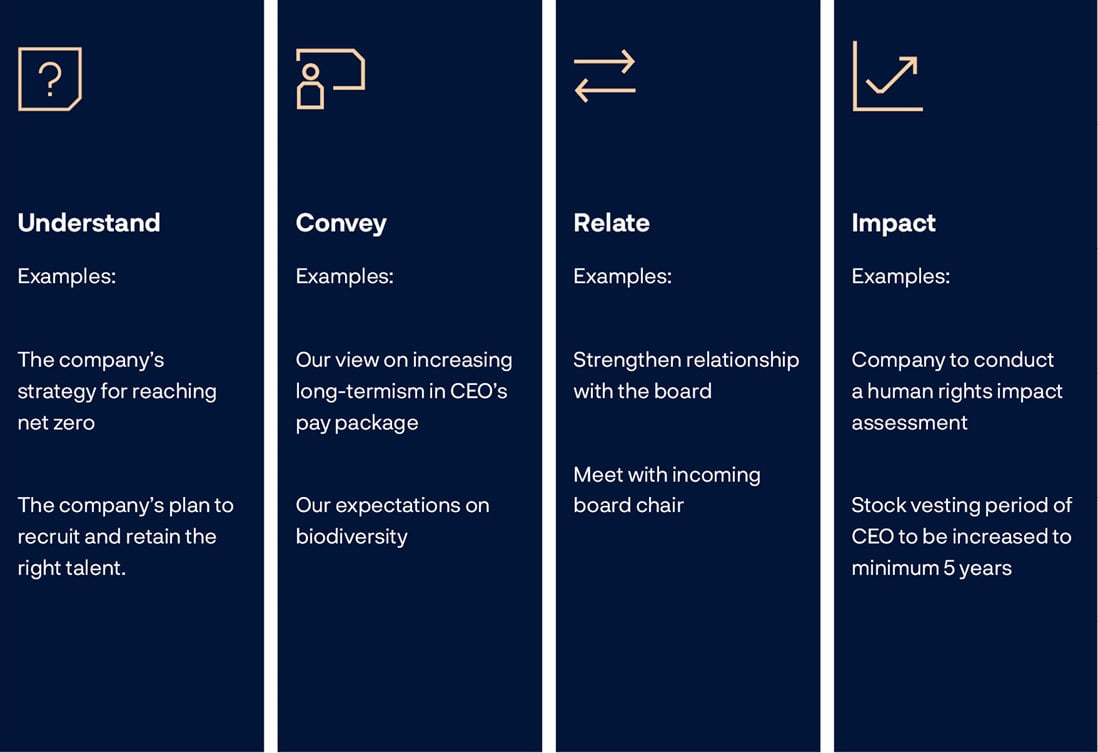

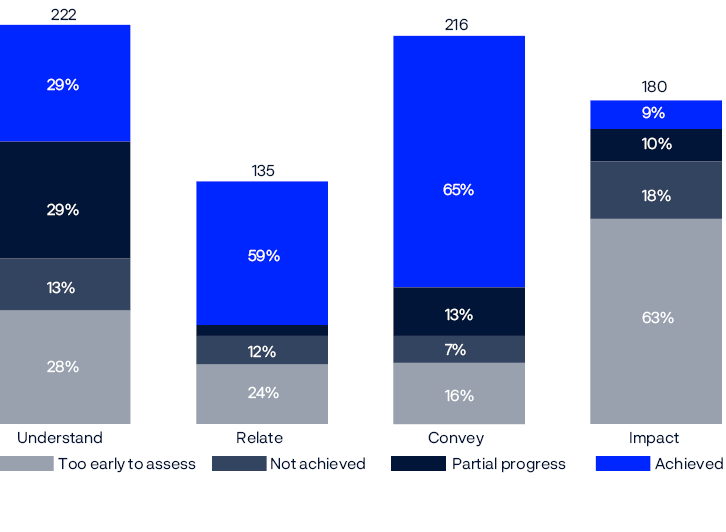

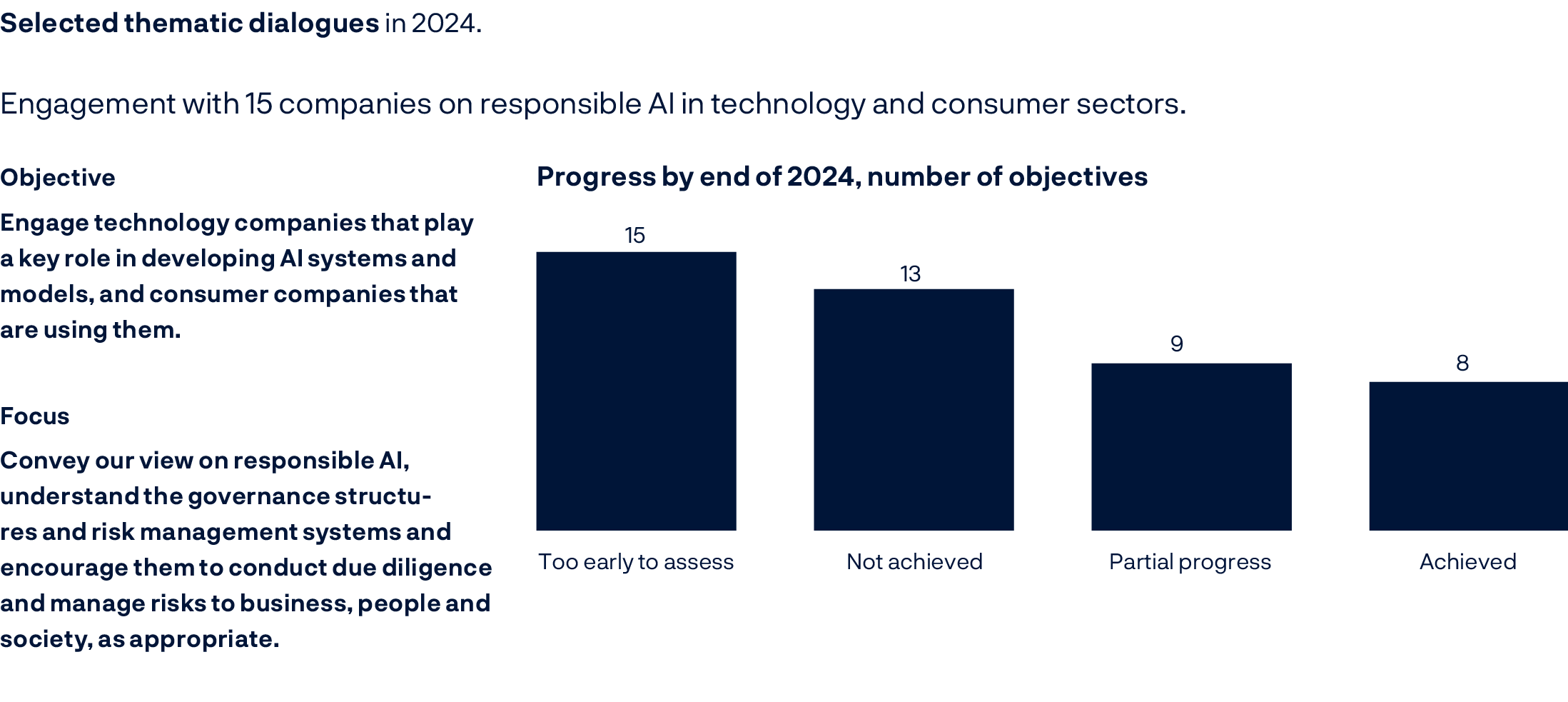

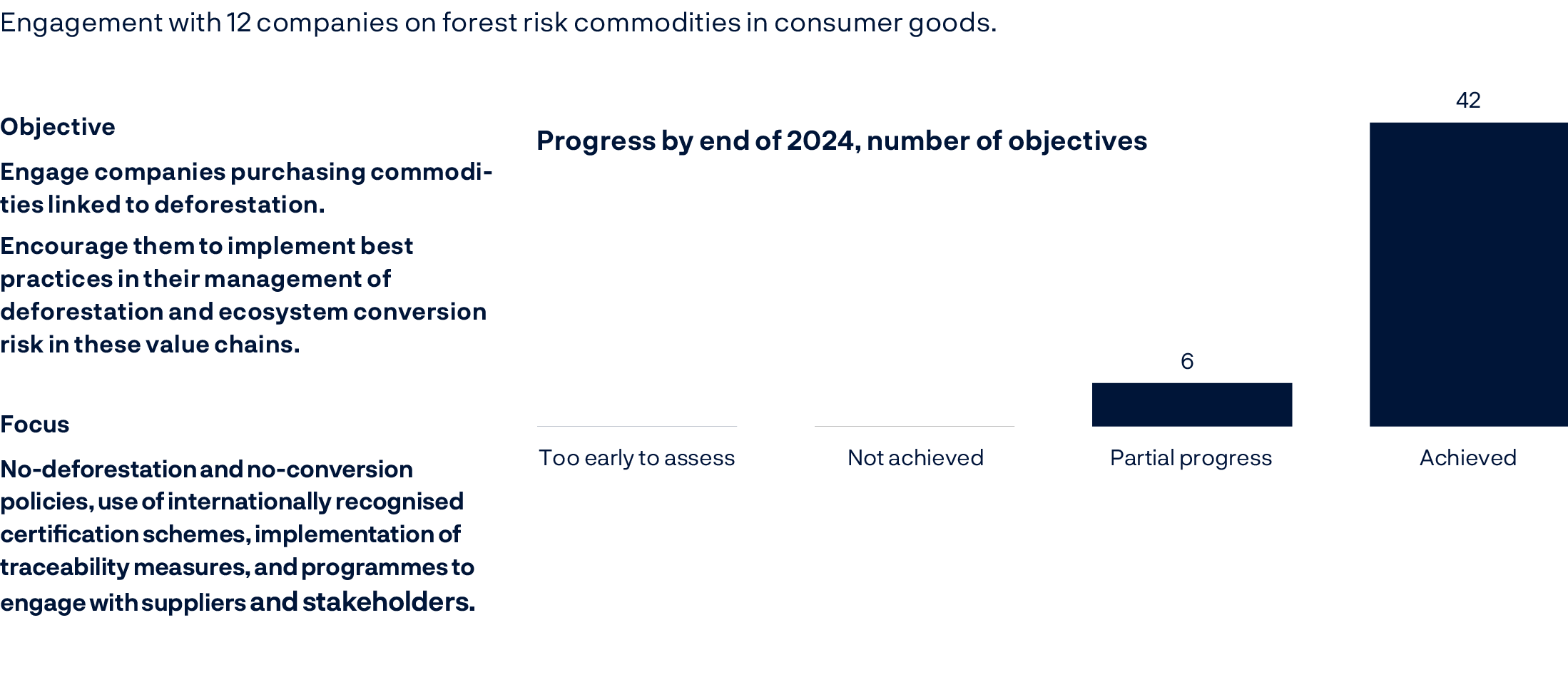

When we initiate a dialogue with a company, we have one or more objectives we want to achieve. These objectives come in a variety of forms based on whether we aim to deepen our understanding, impact a particular practice, build a better relationship, or convey our views. Before engaging with a company on governance or sustainability issues, we formulate one or more objectives and plan engagements around them. We use a system to track our interactions and progress towards our objectives, helping us understand them better and eventually, report more extensively on their impact.

Examples of our objectives in a dialogue

Strategic board dialogues

For our strategic board dialogues, we meet the boards of our largest holdings with the aim of enhancing our understanding of the company and improving our investment performance. We seek to understand the company and board better, and to support the role of the board by conveying our views and investment perspectives directly, over time. The meetings are held with the chair or another leading board member and attended on our side by the investment and active ownership teams. We see benefits in having our portfolio managers present at these meetings. Hearing the views of the board, together with the information we get from management at other meetings, gives us a better insight into the company and can improve the quality of our investment decisions.

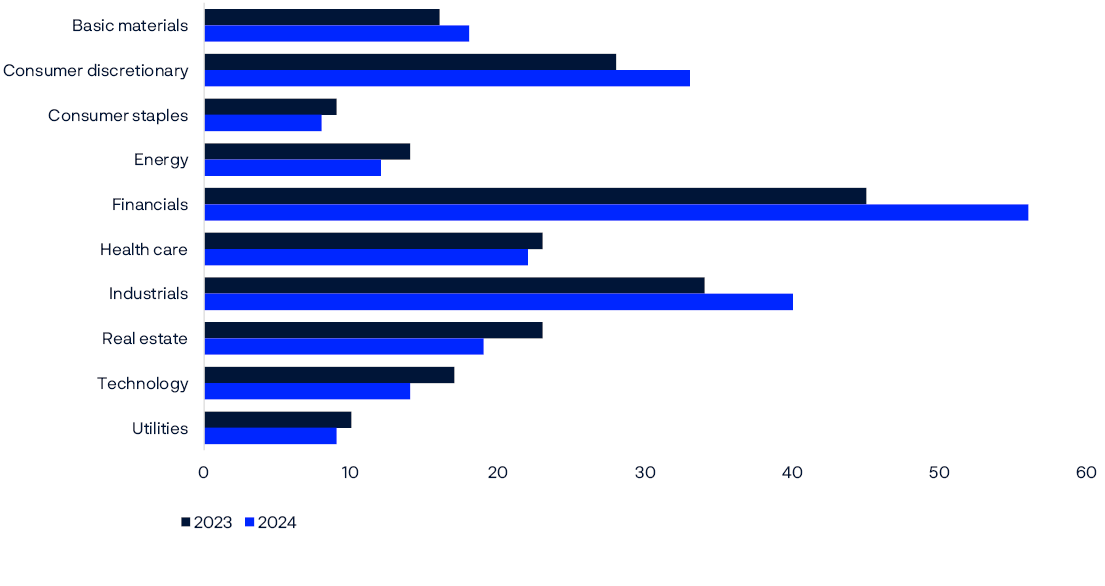

In addition to our strategic board dialogues, we hold many more board-level meetings with portfolio companies, as part of our regular, net zero and thematic dialogues. Overall, in 2024, we had 234 meetings at board level, with 179 companies. These companies accounted for 25 percent of the equity portfolio by value.

Examples of strategic board dialogues in 2024 and some of the topics we discussed.

|

Company |

Sector |

Agenda |

|||

|---|---|---|---|---|---|

|

AstraZeneca PLC |

Health care |

Board composition |

Succession planning |

Remuneration |

Strategy |

|

Capgemeni SE |

Technology |

||||

|

Vonovia SE |

Real estate |

Capital management |

|||

|

Schneider Electric SE |

Industrials goods and services |

Human capital |

|||

|

Sanofi SA |

Health care |

Strategy |

|||

|

Exxon Mobil Corp |

Energy |

Shareholder rights |

Capital management |

||

|

Anglo American Plc |

Basic resources |

||||

|

Tesla Inc |

Consumer discretionary |

Remuneration |

Human rights |

||

|

McDonald's Corp |

Consumer discretionary |

Strategy |

Human capital |

||

Number of meetings held with company boards by sector in 2023 and 2024.

Net zero dialogues

A core part of our 2025 Climate Action Plan is to engage with the highest emitters in our portfolio on their plans for achieving net zero emissions by 2050. In line with our financial interests, we want to support our portfolio companies in delivering long-term financial value, and adapting their business models.

We have included these high-emitting companies on a focus list. The list includes 70 percent of financed scope 1 and scope 2 emissions from the companies in the equity portfolio, our largest investments in sectors with significant indirect exposure to climate risk, and additional companies with elevated climate risk based on proprietary assessments. Climate considerations are integrated into all relevant engagements we have with these companies.

We conduct detailed dialogues by sector with companies on the focus list, discussing their climate targets, transition plans and emission reductions. We set and track specific objectives for each dialogue and company, based on their plans and progress versus peers. Dialogues often start with us establishing deeper relationships with the companies, understanding nuances in their decarbonisation strategies and conveying our general expectations. Where relevant, we then set impact objectives for specific and value-enhancing changes we want to see at the companies. These objectives may for instance relate to the companies’ targets, strategies, governance framework or disclosures.

In 2024, we made progress on our sector-specific engagements, and started new ones with cement companies, insurance companies and pulp and paper companies. Examples of objectives we have reached are companies setting net zero 2050 targets, conveying our expectations on scope 3 emissions and getting a better understanding of companies’ transition plans.